The WPJ

Residential Real Estate News

Renters in U.S. Becoming More Skeptical About Home Ownership in Q3

According to the National Association of Realtors' Housing Opportunities and Market Experience (HOME) survey, lofty U.S. home-price growth and tight supply are leading to softening confidence among renters about whether it's a good time to buy a home or not.

In NAR's third quarter HOME consumer survey, respondents were asked about their confidence in the U.S. economy and various questions about their housing expectations, including a series of questions related to down payments and the amount of money they believe they need to purchase a home.

Heading into the autumn months of 2016, the share of homeowners and renters who believe now is a good time to buy remains at a solid majority but has crept downward since the beginning of this year. Seventy-eight percent of homeowners (80 percent in June; 82 percent in March) and 60 percent of renters (62 percent in the previous two quarters) said it's a good time to buy. In the inaugural HOME survey in December 2015, 68 percent of renters said it was a good time to buy.

Lawrence Yun, NAR chief economist, says it's clear the ongoing run-up in home prices and severe inventory shortages in a large portion of the country are hitting consumer psyche - especially among renters. "This summer's historically low mortgage rates injected some additional demand into the market, but the dearth of homes for sale continues to keep a lid on sales but not prices," he said. "Given the stiff competition and limited homes available at the lower end of the market, it's not surprising at all that those under the age of 34 and in the West are the least confident about it being a good time to buy."

Adds Yun, "Very affordable mortgage rates and strong job gains among young adults should be translating to a higher rate of homeownership. It's not, and as a result, sales to first-time buyers remain stuck below a third of all sales."

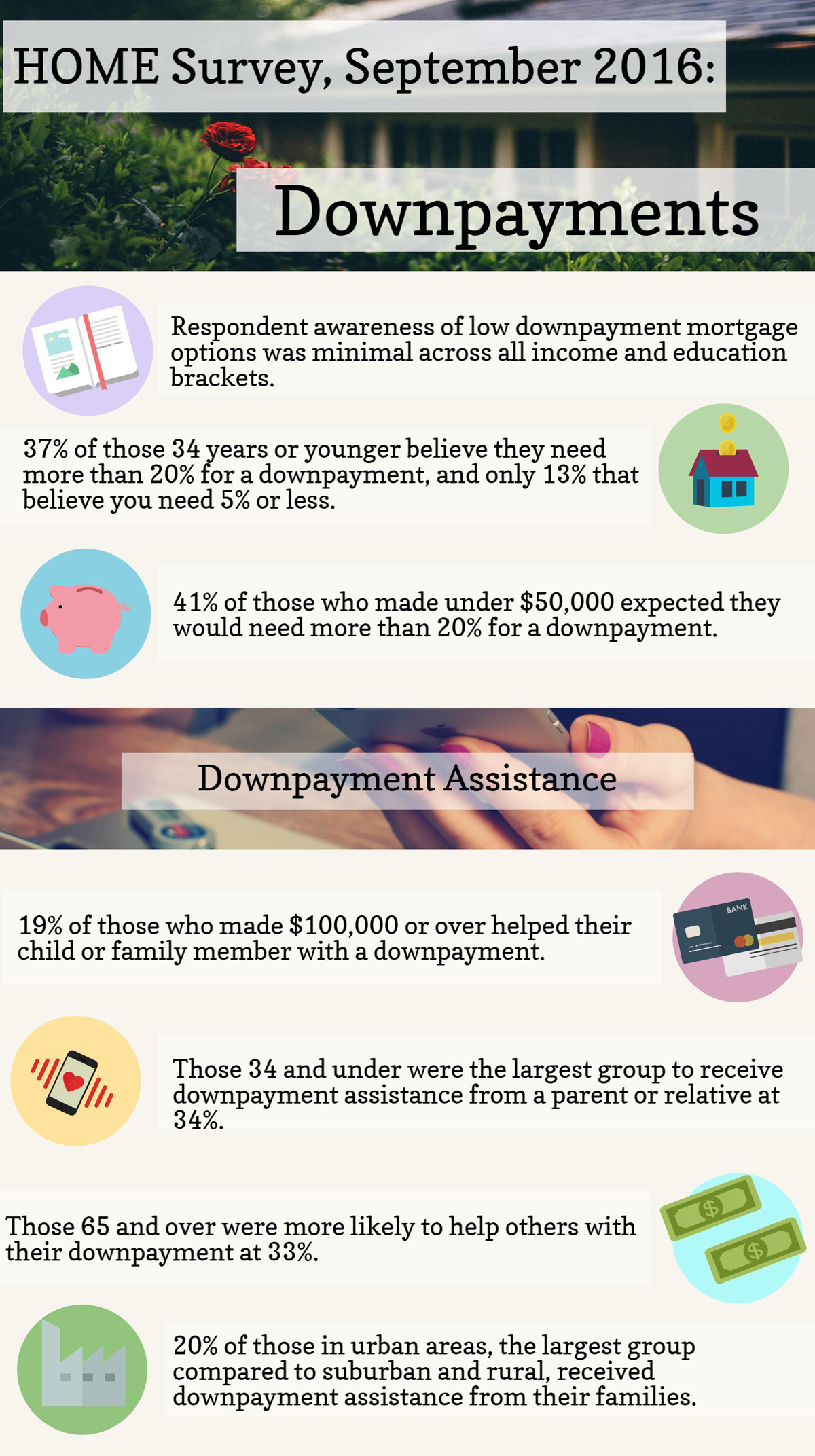

This quarter's HOME survey also found that awareness of low-down-payment mortgage options was scarce across all ages, income brackets and education levels. Fewer than 20 percent in each group indicated that they need 10 percent or less to finance their home purchase. Those ages 65 and older (43 percent) and under the age of 35 (37 percent) were the most likely to believe that they need more than 20 percent.

"It's possible some of the hesitation about buying right now among young adults is from them not realizing there are mortgage financing options available that do not require a 20 percent down payment, which would be north of $100,000 in some expensive areas in the country," says Yun. "In fact, most first-time buyers put down much less. In the 35 year history of NAR's Profile of Home Buyers and Sellers - the longest-running survey series of national housing data - the average median down payment has been 5 percent for first-time buyers."

With home prices and rents continuing to climb and make it difficult for many to save for a home purchase, one avenue for about a fifth (19 percent) of current homeowners was receiving down payment assistance from a parent or relative. Homeowners ages 34 and under were the most likely to say they received help from a parent or relative (34 percent), along with those living in the Northeast and in urban areas.

When it comes to giving aid to prospective buyers, 16 percent said they have helped a child or relative with their down payment. It's no surprise that the older the respondent, the more likely they were to assist.

"Creditworthy prospective buyers should know that many lenders now offer safe, sustainable loans with as little as 3 percent down, and obtaining a mortgage isn't as difficult as it was in the immediate years after the downturn," says NAR President Tom Salomone. "Every buyer is different. Before deciding how much to use on a down payment, buyers should carefully review their financial situation and make sure they still have enough money set aside after the home purchase for unexpected expenses and emergencies."

Feelings about direction of U.S. economy, personal financial outlook remain unchanged

Following the same trend line since the inaugural HOME survey in December 2015, a little less than half of all households in the survey believe the economy is improving (48 percent). The younger the household the more optimistic they were about the economy's future prospects. Meanwhile, nearly two-thirds of those living in rural areas (63 percent) and 61 percent of those over the age of 65 don't believe the economy is improving.

The HOME survey's monthly Personal Financial Outlook Index, showing respondents' confidence that their financial situation will be better in six months, ticked up very slightly (to 58.6 in September) since June (57.7), but is up much more since last September, when stock market losses at the time temporarily caused more consumer angst (53.0).

Most expect prices to hold steady or increase, slightly more think it's a good time to sell

More current homeowners (63 percent) believe it is a good time to sell compared to the second quarter of this year (61 percent). Respondents in the West continue to be the most likely to think now is a good time to sell, while also being the least likely to think now is a good time to buy.

Consistent with last quarter (93 percent), almost all of those surveyed (91 percent) believe that prices will stay the same or rise in their community in the next six months. Renters, respondents living in urban areas and those from the West are most likely to believe prices will go up in their communities.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More