The WPJ

Commercial Real Estate News

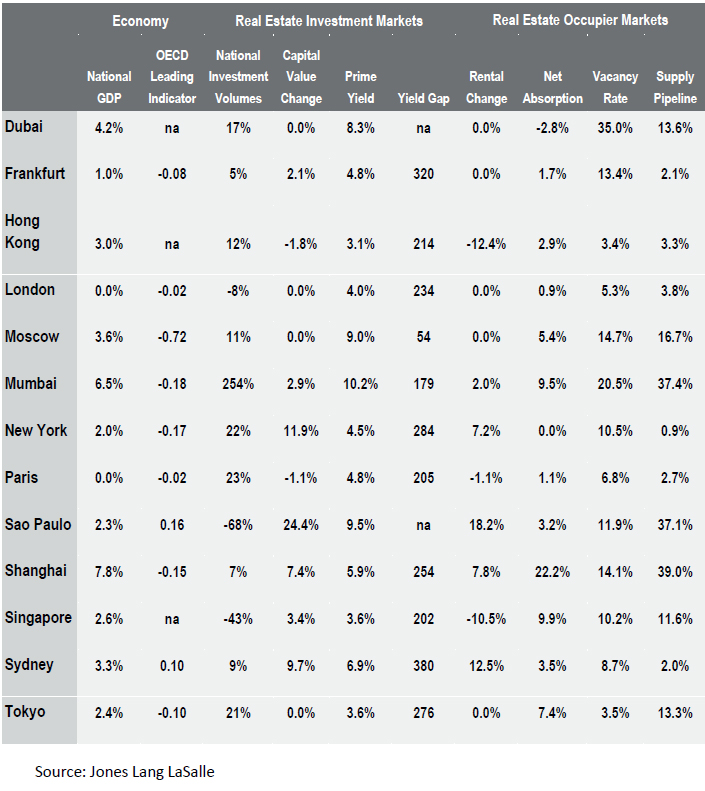

Global Commercial Property Markets Emerging From Economic Fog in 2Q, Says New JLL Report

This week global real estate consulting firm Jones Lang LaSalle (JLL) released thier second quarter Global Market Perspective, which captures in-depth data and analysis on the global property market in the year to date.

This week global real estate consulting firm Jones Lang LaSalle (JLL) released thier second quarter Global Market Perspective, which captures in-depth data and analysis on the global property market in the year to date.According to the report, following a lull in activity during Q1, the global property market has resumed a steady recovery path. Investment volumes recovered to US$108 billion in Q2, up 24 percent quarter over quarter, signaling that capital markets are on track to achieving US$400 billion volumes for full-year 2012.

Josh Gelormini, Vice President of Research at Jones Lang LaSalle tells World Property Channel, "In the office leasing markets, a combination of corporate relocation, consolidation, and - very selectively - specific industry-related expansion is continuing to motor measured improvement globally."

Gelormini further continues, "Meanwhile, investors continue to seek opportunities to purchase well-located core product across a diverse mix of cities and property types, motivated in large part by attractive relative yields, compared with other asset classes."

Other key JLL global market highlights in 2Q include:

- The global economic outlook has weakened as euro strains re-emerge. Asia Pacific markets will continue to drive global growth this year, however, a deceleration is increasingly apparent.

- In a climate of uncertainty, corporate occupiers have adopted a "wait and see" approach to expansion as global take-up volumes have fallen year-on-year. Corporates are trending towards sale and leaseback transactions as they look to release capital.

- Leasing activities have improved from the Q1 lull, but are still below 2011 levels due to weak jobs growth, slow corporate hiring and the downward reset of global growth projections. Gross leasing volumes for full-year 2012 expected to be 10 percent lower than in 2011.

- On the other hand, vacancy continues to edge downwards, with the global office vacancy rate falling to 13.3 percent in Q2, the lowest since 2009. Regionally, the Americas and Asia Pacific regions have continued to see vacancy rates fall, while they have remained unchanged in Europe.

- With global office supply still falling, the Jones Lang LaSalle Global Office Index, which tracks the rental performance of prime office space across 90 major markets, has continued to grow, up by a further 0.6 percent during Q2 2012.

- In residential, high trading volumes have been recorded for Germany, while momentum has been maintained in the U.S. rental apartment market. In Asia, residential sales have improved in China and Hong Kong and remain resilient in Jakarta, driven by investor interest, low lending rates and rising rental returns.

- Retail exhibited a mixed picture. While Greater China recorded strong demand and healthy rental growth, market conditions were relatively flat in the US. In Europe, demand is expected to drive rents in the top retail locations in London, Moscow and Paris in the second half of 2012, while most other European markets will remain broadly stable.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More