The WPJ

Commercial Real Estate News

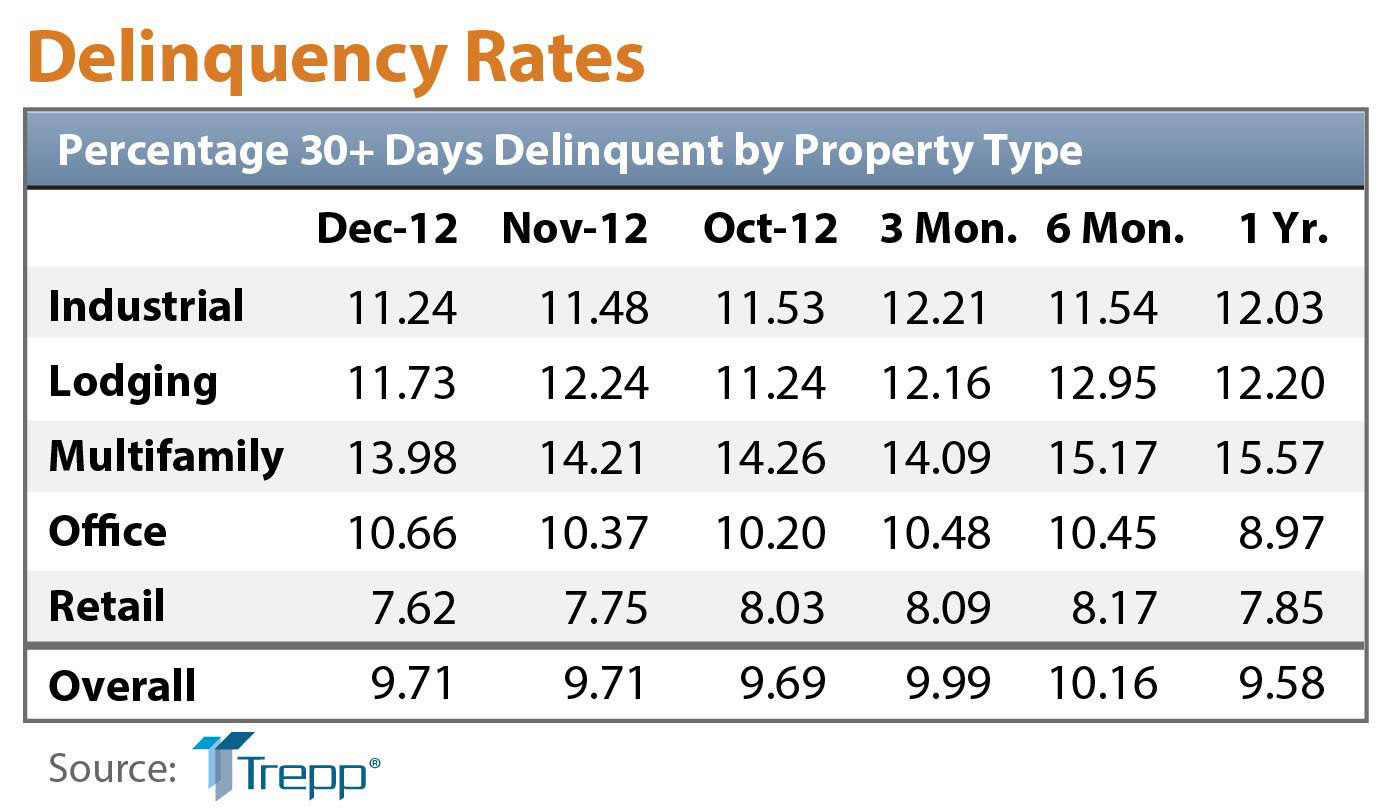

CMBS Delinquency Rates in U.S. Unchanged in December

According to Trepp, CMBS delinquency rate in December was unchanged from the previous month at 9.71%. After months of continued volatility, the delinquency rate for US commercial real estate loans in CMBS has regained some stability. From early 2012 through the end of the summer, the CMBS delinquency rate bounced around considerably.

According to Trepp, CMBS delinquency rate in December was unchanged from the previous month at 9.71%. After months of continued volatility, the delinquency rate for US commercial real estate loans in CMBS has regained some stability. From early 2012 through the end of the summer, the CMBS delinquency rate bounced around considerably.Large movements in the delinquency rate during the first six months of the year were caused primarily by the high number of five-year loans securitized in 2007. As these loans reached their maturity dates and were unable to refinance, the rate was pushed to record highs. With these troubled loans now behind the market and the next wave not coming due until 2014, rate movements should be modest in the near future.

Forward-looking data suggests the rate will see further improvement in the coming months. Special servicers are continuing to resolve non-performing loans and new CMBS deals are being added to the index, diluting the pool of non-performers.

The number of newly delinquent loans decreased from November to December, totaling around $3.2 billion last month. While there were fewer new delinquencies, the number of delinquent loans resolved with losses also decreased, with just over $1.1 billion resolved.

Among the major property types, office was the only segment to see a higher delinquency percentage in December. Loans backed by offices saw their rate jump 29 basis points last month. This weakness was enough to offset gains in other major property types.

"Despite the fact that the delinquency rate has leveled off once again, it's been a spectacular run for the CMBS industry over the last six months," said Manus Clancy, senior managing director of Trepp. "Not only did the world not end on December 21, but spreads have plummeted since June, it's become easier for borrowers to refinance, research groups are lifting their estimates for 2013 issuance, and delinquency rates are well below their all-time highs."

While Trepp anticipates the delinquency rate will be steady over the next few months, refinancings are expected to increase as a result of borrowing rates and CMBS spreads being at record lows. Additional refinancing activity will lead to the removal of some performing loans.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More