The WPJ

Residential Real Estate News

Data Shows Dramatic Drop in U.S. Foreclosures

Foreclosure filings in the United States are down 25 percent from a year ago, prompting speculation that housing markets may be returning to a semblance of normalcy.

"At a high level the U.S. foreclosure inferno has been effectively contained and should be reduced to a slow burn in the next two years," said Daren Blomquist, vice president of RealtyTrac, which released the latest data.

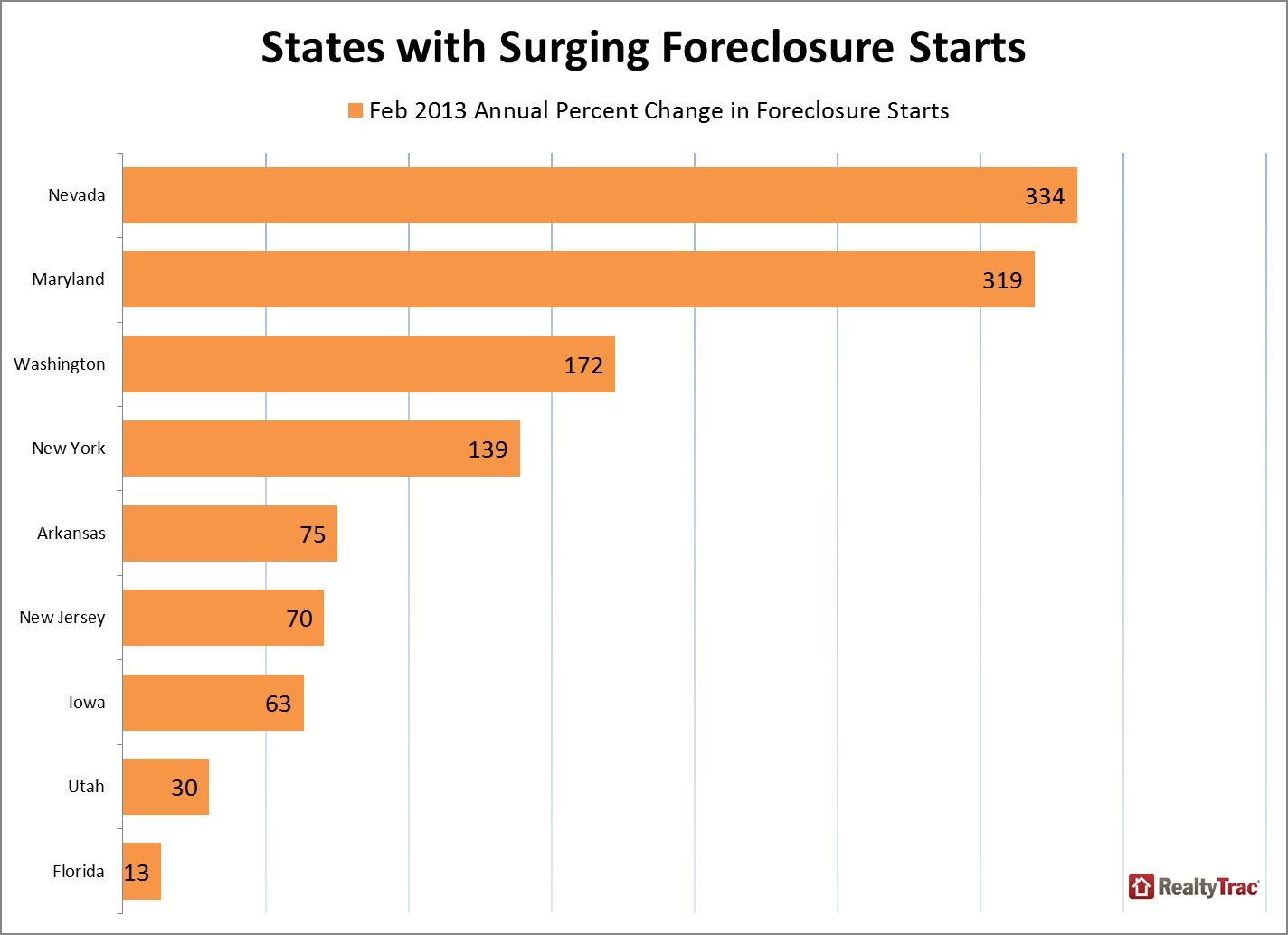

"At a high level the U.S. foreclosure inferno has been effectively contained and should be reduced to a slow burn in the next two years," said Daren Blomquist, vice president of RealtyTrac, which released the latest data.However, the news was not all positive. Foreclosure starts in February increased 10 percent from the previous month after three consecutive monthly decreases. Foreclosure starts increased from the previous month in 32 states and were up from a year ago in 16 states, including Nevada, Maryland, Washington, New York and New Jersey.

More from Mr. Blomquist:

"Dangerous foreclosure flare-ups are still popping up in states where foreclosures have been delayed by a lengthy court process or by new legislation making it more difficult to foreclose outside of the court system. Foreclosure starts have been steadily building in those states over the last several months and likely will end up as bank repossessions or short sales later this year.

"Dangerous foreclosure flare-ups are still popping up in states where foreclosures have been delayed by a lengthy court process or by new legislation making it more difficult to foreclose outside of the court system. Foreclosure starts have been steadily building in those states over the last several months and likely will end up as bank repossessions or short sales later this year."These new foreclosure hot spots include states like Washington, where seven straight months of rising foreclosure activity pushed the state's foreclosure rate to fifth highest nationwide --the highest it's ever been in our report -- and Maryland, where eight straight months of rising foreclosure activity placed the state's foreclosure rate among the top 10 nationwide for the first time since July 2010."

Florida is still struggling with foreclosures, according to the data. The Sunshine State posted the nation's highest state foreclosure rate for the sixth consecutive month in February, reporting one in every 282 housing units with a foreclosure filing during the month. And Florida cities accounted for seven of the nation's 10 highest metro foreclosure rates in February, led by the Miami, Orlando, Ocala, Tampa and Palm Bay metro areas, according to RealtyTrac data.

Watch RealtyTrac's report:

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More