The WPJ

Residential Real Estate News

U.S. Home Prices Enjoy Biggest Percentage Increase in 7 Years, Low Inventory and Rates Driving Market

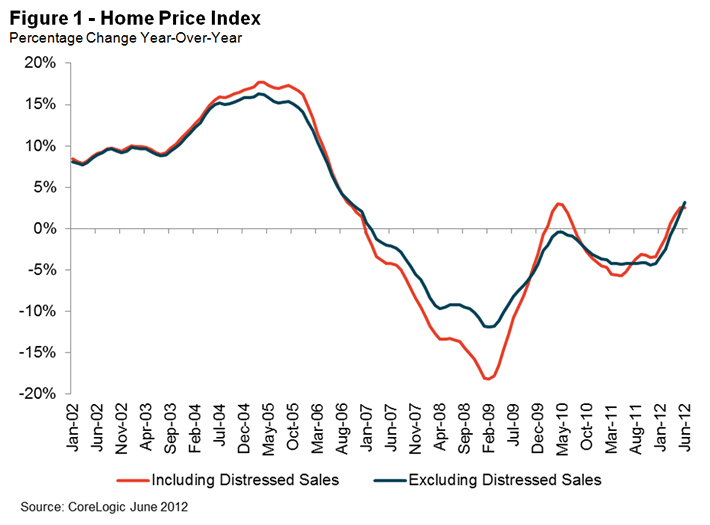

According to CoreLogic's June Home Price Index (HPI) report, home prices nationwide, including distressed sales, increased on a year-over-year basis by 2.5 percent in June 2012 compared to June 2011.

According to CoreLogic's June Home Price Index (HPI) report, home prices nationwide, including distressed sales, increased on a year-over-year basis by 2.5 percent in June 2012 compared to June 2011.On a month-over-month basis, including distressed sales, home prices increased by 1.3 percent in June 2012 compared to May 2012. The June 2012 figures mark the fourth consecutive increase in home prices nationally on both a year-over-year and month-over-month basis.

Excluding distressed sales, home prices nationwide increased on a year-over-year basis by 3.2 percent in June 2012 compared to June 2011. On a month-over-month basis excluding distressed sales, home prices increased 2.0 percent in June 2012 compared to May 2012, the fifth consecutive month-over-month increase. Distressed sales include short sales and real estate owned (REO) transactions.

The CoreLogic Pending HPI indicates that July home prices, including distressed sales, will rise by at least 0.4 percent on a month-over-month basis from June 2012 and by 2.0 percent on a year-over-year basis from July 2011. Excluding distressed sales, July house prices are also poised to rise by 1.4 percent month-over-month from June 2012 and by 4.3 percent year-over-year from July 2011.

"Home prices are responding positively to reductions in both visible and shadow inventory over the past year," said Mark Fleming, chief economist for CoreLogic. "This trend is a bright spot because the decline in shadow inventory translates to fewer distressed sales, which helps sustain price appreciation."

"At the halfway point, 2012 is increasingly looking like the year that the residential housing market may have turned the corner," said Anand Nallathambi, president and CEO of CoreLogic. "While first-half gains have given way to second-half declines over the past three years, we see encouraging signs that modest price gains are supportable across the country in the second-half of 2012."

Highlights as of June 2012:

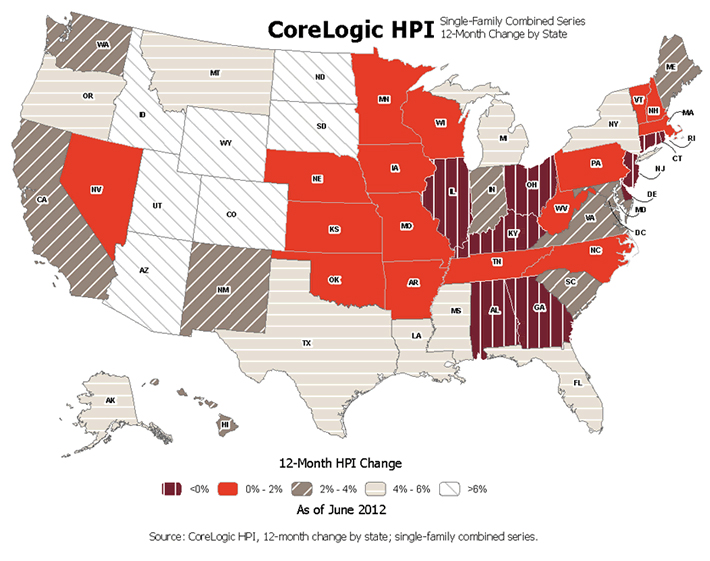

- Including distressed sales, the five states with the highest appreciation were: Arizona (+13.8 percent), Idaho (10.4 percent), South Dakota (+10.1 percent), Utah (+8.3 percent) and Wyoming (+7.7 percent).

- Including distressed sales, the five states with the greatest depreciation were: Alabama (-4.8 percent), Connecticut (-4.0 percent), Illinois (-3.4 percent), Georgia (-2.9 percent) and Delaware (-2.8 percent).

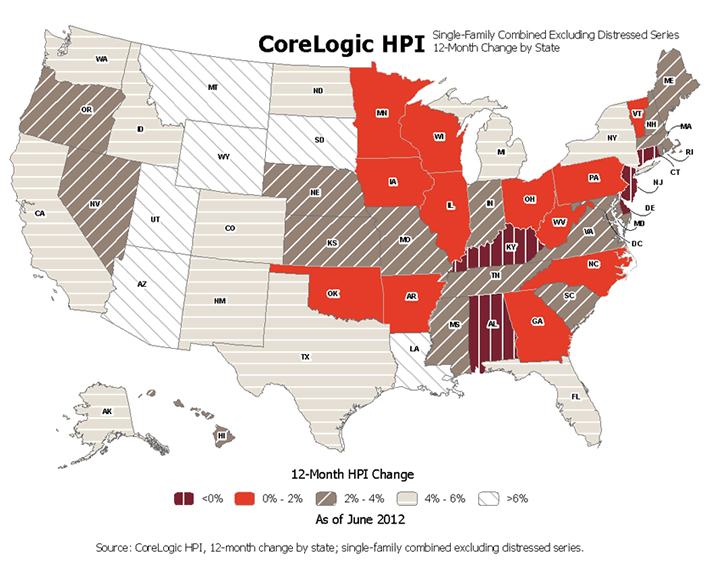

- Excluding distressed sales, the five states with the highest appreciation were: South Dakota (+10.2 percent), Utah (+9.1 percent), Montana (+8.7 percent), Arizona (+8.7 percent) and Wyoming (+6.9 percent).

- Excluding distressed sales, the five states with the greatest depreciation were: Delaware (-3.6 percent), Alabama (-3.1 percent), Connecticut (-2.1 percent), New Jersey (-0.9 percent) and Kentucky (-0.4 percent).

- Including distressed transactions, the peak-to-current change in the national HPI (from April 2006 to June 2012) was -28.8 percent. Excluding distressed transactions, the peak-to-current change in the HPI for the same period was -21.3 percent.

- The five states with the largest peak-to-current declines including distressed transactions are Nevada (-57.1 percent), Florida (-45.3 percent), Arizona (-44.1 percent), California (-39.2 percent) and Michigan (-39.0 percent).

- Of the top 100 Core Based Statistical Areas (CBSAs) measured by population, 27 are showing year-over-year declines in June, five fewer than in May.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More