The WPJ

Residential Real Estate News

U.S. Home Prices Rise for Third Consecutive Month, Says Corelogic Index

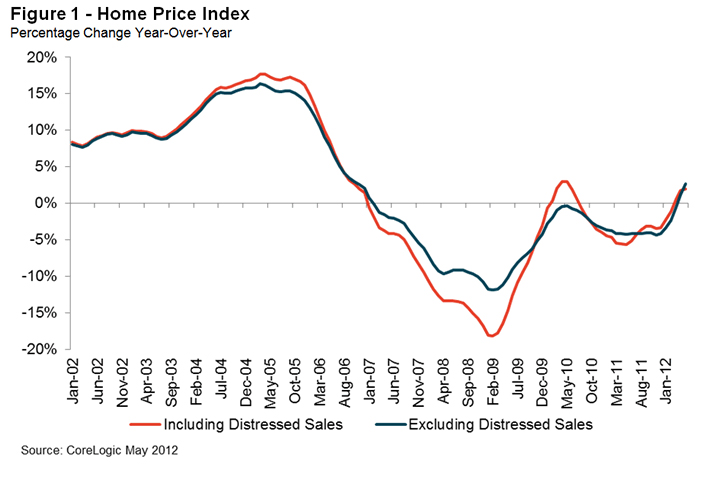

According to CoreLogic's May Home Price Index (HPI) report, home prices nationwide, including distressed sales, increased on a year-over-year basis by 2.0 percent in May 2012 compared to May 2011.

According to CoreLogic's May Home Price Index (HPI) report, home prices nationwide, including distressed sales, increased on a year-over-year basis by 2.0 percent in May 2012 compared to May 2011.On a month-over-month basis, home prices, including distressed sales, also increased by 1.8 percent in May 2012 compared to April 2012. The May 2012 figures mark the third consecutive increase in home prices nationwide on both a year-over-year and month-over-month basis.

Excluding distressed sales, home prices nationwide increased on a year-over-year basis by 2.7 percent in May 2012 compared to May 2011. On a month-over-month basis excluding distressed sales, the CoreLogic HPI indicates home prices increased 2.3 percent in May 2012 compared to April 2012, the fourth month-over-month increase in a row. Distressed sales include short sales and real estate owned (REO) transactions.

The CoreLogic Pending HPI indicates that house prices, including distressed sales, will rise by at least another 1.4 percent from May 2012 to June 2012. Excluding distressed sales, house prices are also poised to rise by 2.0 percent during that same time period. The CoreLogic Pending HPI is a new and exclusive metric that was introduced within the April 2012 HPI report. It provides the most current indication of trends in home prices, and is based on Multiple Listing Service (MLS) data that measure price changes in the most recent month.

"The recent upward trend in U.S. home prices is an encouraging signal that we may be seeing a bottoming of the housing down cycle," said Anand Nallathambi, president and chief executive officer of CoreLogic. "Tighter inventory is contributing to broad, but modest, price gains nationwide and more significant gains in the harder-hit markets, like Phoenix."

"Home price appreciation in the lower-priced segment of the market is rebounding more quickly than in the upper end," said Mark Fleming, chief economist for CoreLogic. "Home prices below 75 percent of the national median increased 5.7 percent from a year ago, compared to only a 1.8 percent increase for prices 125 percent or more of the median."

Highlights as of May 2012

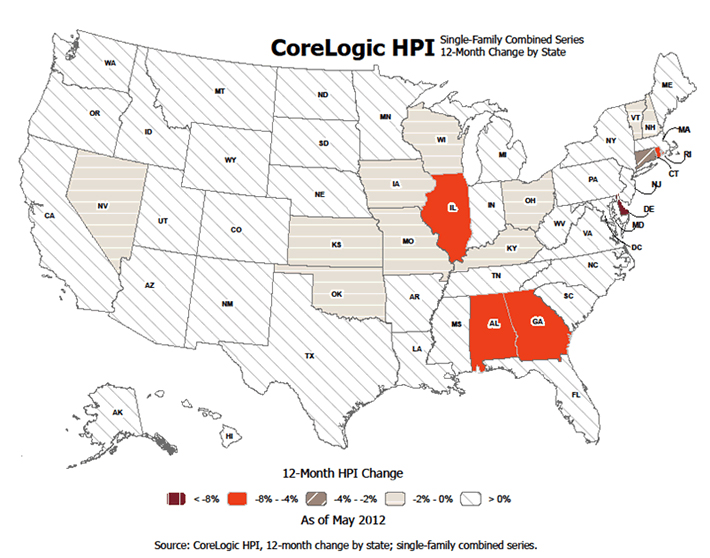

- Including distressed sales, the five states with the highest appreciation were: Arizona (+12.0 percent), Idaho (+9.2 percent), South Dakota (+8.7 percent), Montana (+8.2 percent) and Michigan (+7.9 percent).

- Including distressed sales, the five states with the greatest depreciation were: Delaware (-9.0 percent), Rhode Island (-4.4 percent), Illinois (-4.2 percent), Alabama (-4.1 percent) and Georgia (-4.0 percent).

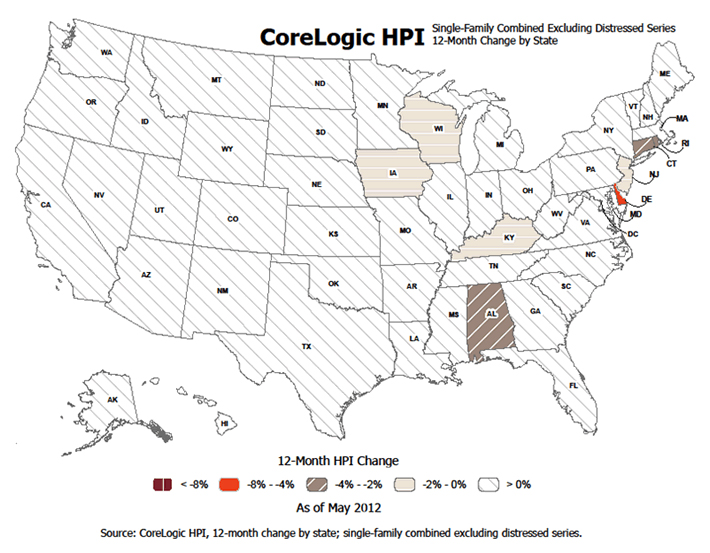

- Excluding distressed sales, the five states with the highest appreciation were: Montana (+9.1 percent), South Dakota (+8.5 percent), Arizona (+7.3 percent), Idaho (+6.6 percent) and Wyoming (+6.6 percent).

- Excluding distressed sales, the five states with the greatest depreciation were: Delaware (-7.8 percent), Rhode Island (-3.8 percent), Alabama (-2.8 percent), Connecticut (-2.2 percent) and Kentucky (-1.2 percent).

- Including distressed transactions, the peak-to-current change in the national HPI (from April 2006 to May 2012) was -30.1 percent. Excluding distressed transactions, the peak-to-current change in the HPI for the same period was -22.2 percent.

- The five states with the largest peak-to-current declines including distressed transactions are Nevada (-57.7 percent), Florida (-45.6 percent), Arizona (-45.0 percent), Michigan (-40.5 percent) and California (-39.7 percent).

- Of the top 100 Core Based Statistical Areas (CBSAs) measured by population, 29 are showing year-over-year declines in May, 12 fewer than in April.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More