The WPJ

Residential Real Estate News

$1.2 Trillion in Negative Homeowner Equity May Be U.S. Entrepreneurism, Job Creators Biggest Headwinds

We all know that the severe downturn in the U.S. housing market, starting in 2007, has unfortunately hurt tens of millions of homeowners, but the 'ripple effect' has become much wider now.

At stake now is both U.S. entrepreneurism and job creation from these new startups.

Given that many young business startups need cash to launch their ventures, coupled with the fact that many U.S. entrepreneurs have historically used their home equity (along with friends and family money) to launch their companies; the last few years of the U.S. housing industry has not been doing them any favors.

This was confirmed by Federal Reserve Chairman Ben Bernanke's Semiannual Monetary Policy Report to the Congress this week.

When the Fed Chairman was asked about the current state of U.S. entrepreneurism, he replied; "There has been a slowdown over the last few years in entrepreneurial business startups, driven by a number of factors, one of which is the loss of homeowners' equity, which many entrepreneurs have leveraged in the past when starting a business."

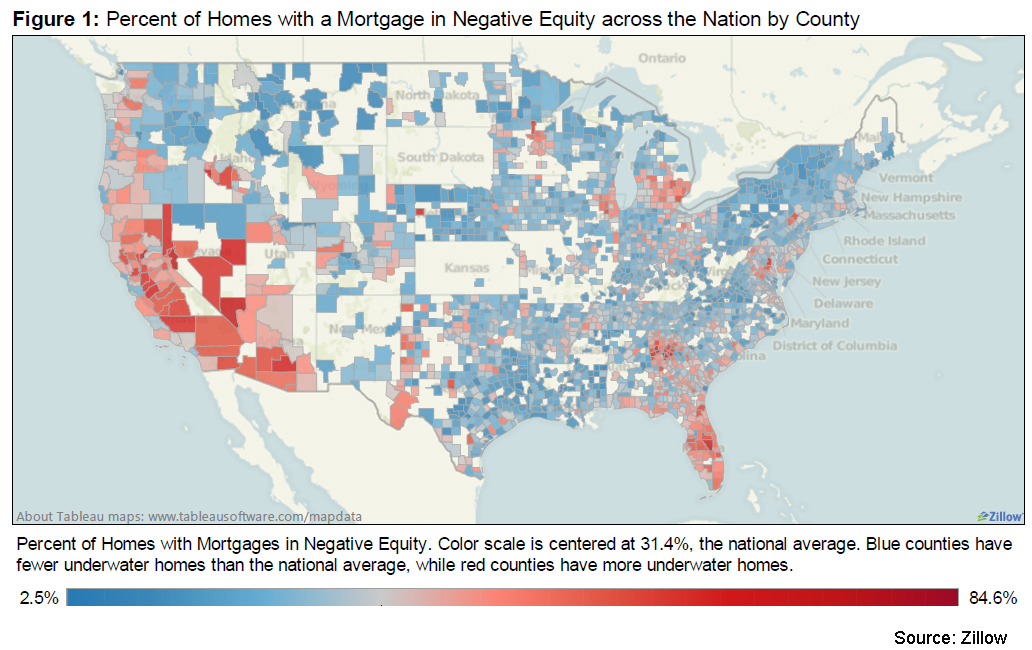

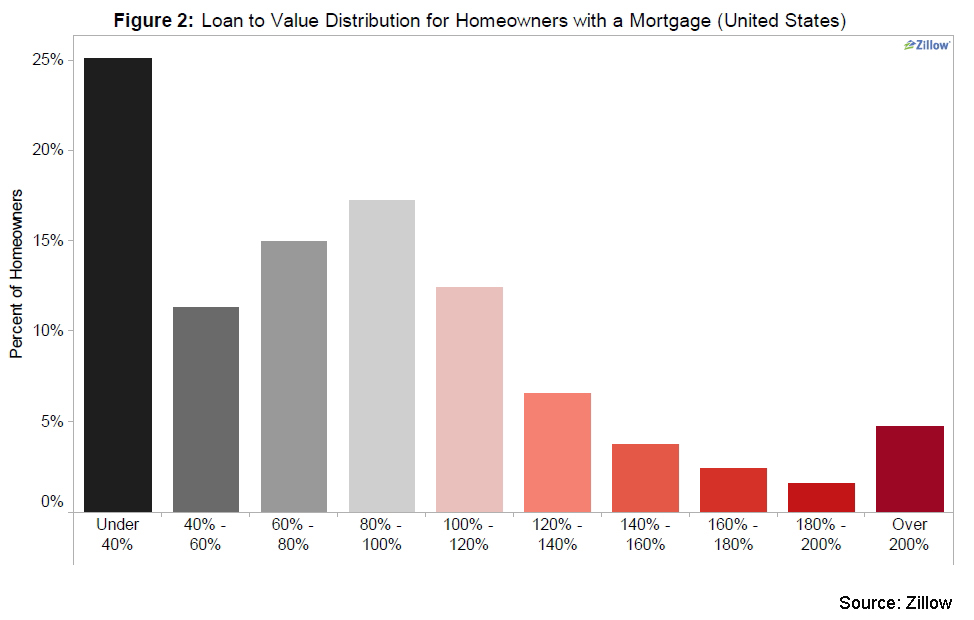

According to Zillow's first quarter 2012 Negative Equity Report, 31.4 percent of U.S. homeowners with a mortgage are underwater (see figure 1). This is nearly flat on a quarterly basis, up only 0.3 percent, but down 1 percent since the first quarter of 2011. On average, U.S. homeowners owe $75,644 more than what their house is worth, or 44.5 percent more. Almost 5 percent of homeowners with a mortgage in the nation owe more than twice what their house is worth (see figure 2). While a third of homeowners with mortgages are underwater, 90 percent of underwater homeowners are current on their mortgage and continue to make payments.

Even though U.S. home prices have started rising in recent quarters, slowly regaining equity losses of the past four years, total negative equity in the U.S. in Q2, 2012 is still around $1.2 Trillion according to Zillow.

The second negative 'ripple-effect' created by negative home owners' equity is directly tied to the first negative effect on entrepreneurism - job creation.

The biggest creators of U.S. jobs for the last several decades have been small business start-ups. With the depletion of their home equity as a funding source, many businesses are not being created now, nor are the millions of possible new jobs that would have come with them.

According to the Kauffman Index of Entrepreneurial Activity March 2012 Report, from 2010 to 2011 entrepreneurial activity rates decreased in all regions of the country except the Northeast, which experienced a slight increase in rates. Entrepreneurship rates are highest in the West and lowest in the Midwest.

Bottom line-- the recent decline in U.S. entrepreneurism is directly impacting U.S. job creation by the millions, as both sectors have been significantly impacted by negative home equity in the U.S.

This trillion-plus dollar loss of homeowner equity may still be the biggest headwind for the recovery of the U.S. housing sector, U.S. entrepreneurism and U.S. job creation for the foreseeable future.

See related news story on WORLD PROPERTY CHANNEL;

Real Estate Listings Showcase

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More