The WPJ

Residential Real Estate News

36,000 Completed U.S. Home Foreclosures in August

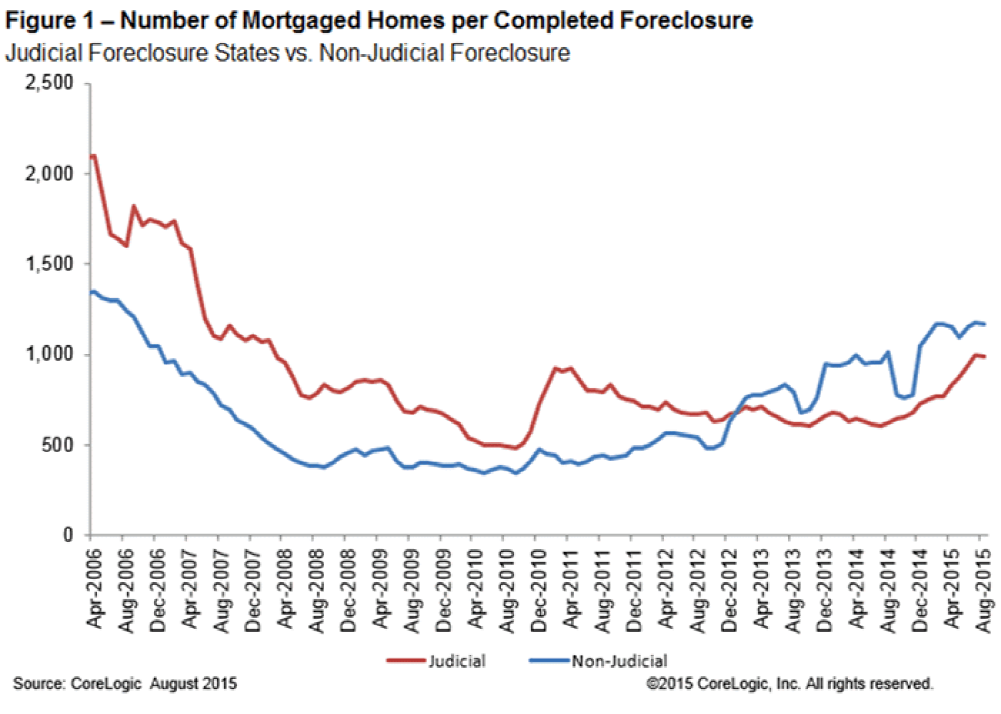

According to CoreLogic's August 2015 National Foreclosure Report, U.S. foreclosure inventory declined by 25.2 percent and completed foreclosures declined by 20.1 percent compared with August 2014. The number of foreclosures nationwide decreased year over year from 46,000 in August 2014 to 36,000 in August 2015, representing a decrease of 68.9 percent from the peak of 117,357 completed foreclosures in September 2010.

Completed foreclosures reflect the total number of homes lost to foreclosure. Since the financial crisis began in September 2008, there have been approximately 5.9 million completed foreclosures across the country, and since homeownership rates peaked in the second quarter of 2004, there have been nearly 8 million homes lost to foreclosure.

As of August 2015, the national foreclosure inventory included approximately 470,000, or 1.2 percent, of all homes with a mortgage compared with 629,000 homes, or 1.6 percent, in August 2014.

CoreLogic also reports that the number of mortgages in serious delinquency (defined as 90 days or more past due, including those loans in foreclosure or REO) declined by 20.7 percent from August 2014 to August 2015 with 1.3 million mortgages, or 3.5 percent, in this category. This is the lowest serious delinquency rate since January 2008. The foreclosure rate (defined as the share of all loans in the foreclosure process) was at 1.2 percent as of August 2015, which is back to January 2008 levels.

"Mortgage performance continues to improve, however there is a dichotomy between the performance of recently originated loans and legacy loans. Newly delinquent loans are at the lowest rates during the last two decades. That reflects the tight underwriting and improved economy during the last few years," said Frank Nothaft, chief economist for CoreLogic. "However, the foreclosure pipeline of legacy loans remains elevated. Over the last 12 months, there have been 500,000 completed foreclosures, more than double the number during normal periods."

"In August, the housing market experienced solid and steady increases in sales, prices and performance and our preview data indicates those trends will continue in September," said Anand Nallathambi, president and CEO of CoreLogic. "Longer term, the recent increase in household formations and rapidly improving labor market for millennials will provide a demographic tailwind to the housing market and keep demand firm."

Additional highlights as of August 2015:

- On a month-over-month basis, completed foreclosures increased minimally, by less than 1 percent, from the 36,000 (rounded) reported in July 2015.* As a basis of comparison, before the decline in the housing market in 2007, completed foreclosures averaged 21,000 per month nationwide between 2000 and 2006.

- The five states with the highest number of completed foreclosures for the 12 months ending in August 2015 were: Florida (94,000), Michigan (47,000), Texas (32,000), California (27,000) and Georgia (26,000). These five states accounted for almost half of all completed foreclosures nationally.

- Four states and the District of Columbia had the lowest number of completed foreclosures for the 12 months ending in August 2015: South Dakota (45), the District of Columbia (116), North Dakota (319), Wyoming (492) and West Virginia (544).

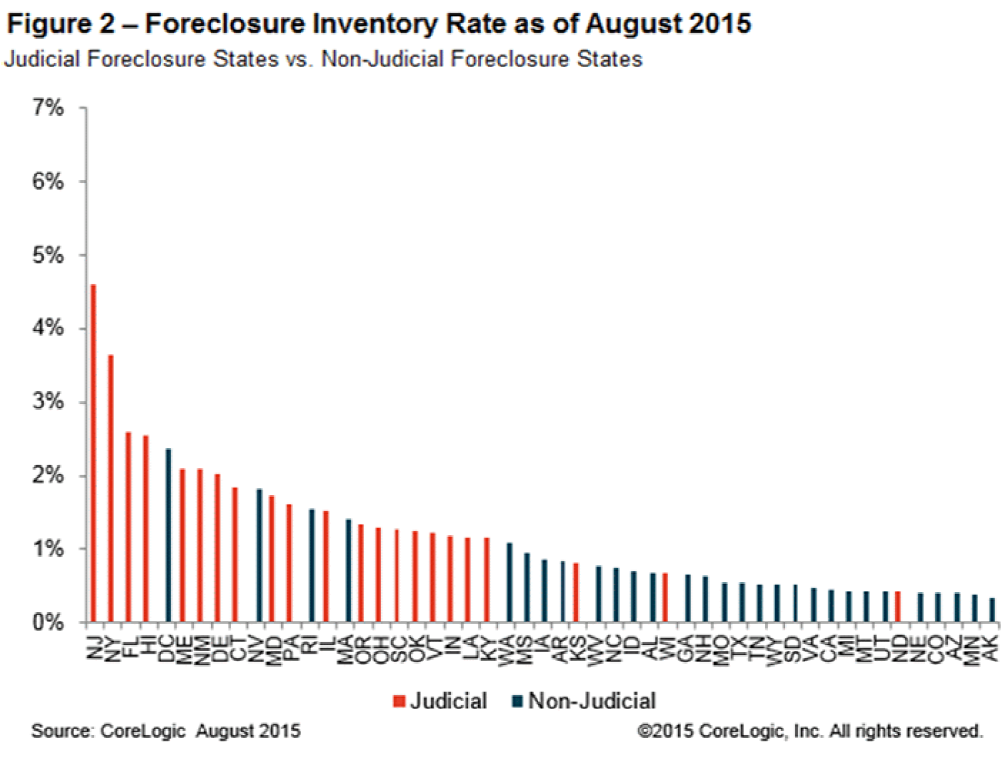

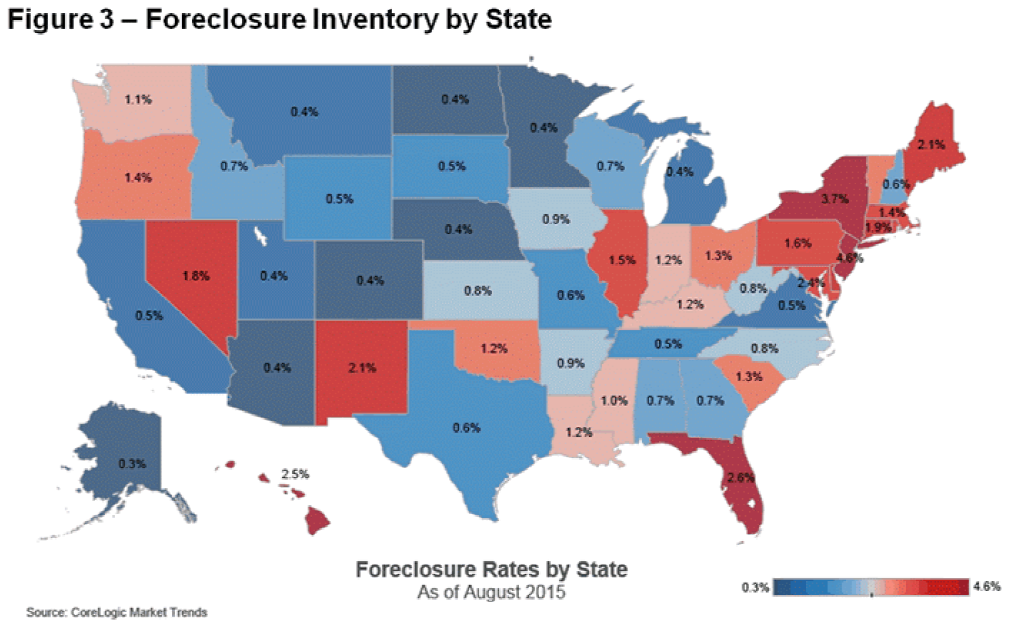

- Four states and the District of Columbia had the highest foreclosure inventory rate as a percentage of all mortgaged homes for the 12 months ending in August 2015: New Jersey (4.6 percent), New York (3.7 percent), Florida (2.6 percent), Hawaii (2.5 percent) and the District of Columbia (2.4 percent).

- The five states with the lowest foreclosure inventory rate as a percentage of all mortgaged homes for the 12 months ending in August 2015 were: Alaska (0.3 percent), Minnesota (0.4 percent), Arizona (0.4 percent), Colorado (0.4 percent) and Nebraska (0.4 percent).

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More