The WPJ

Residential Real Estate News

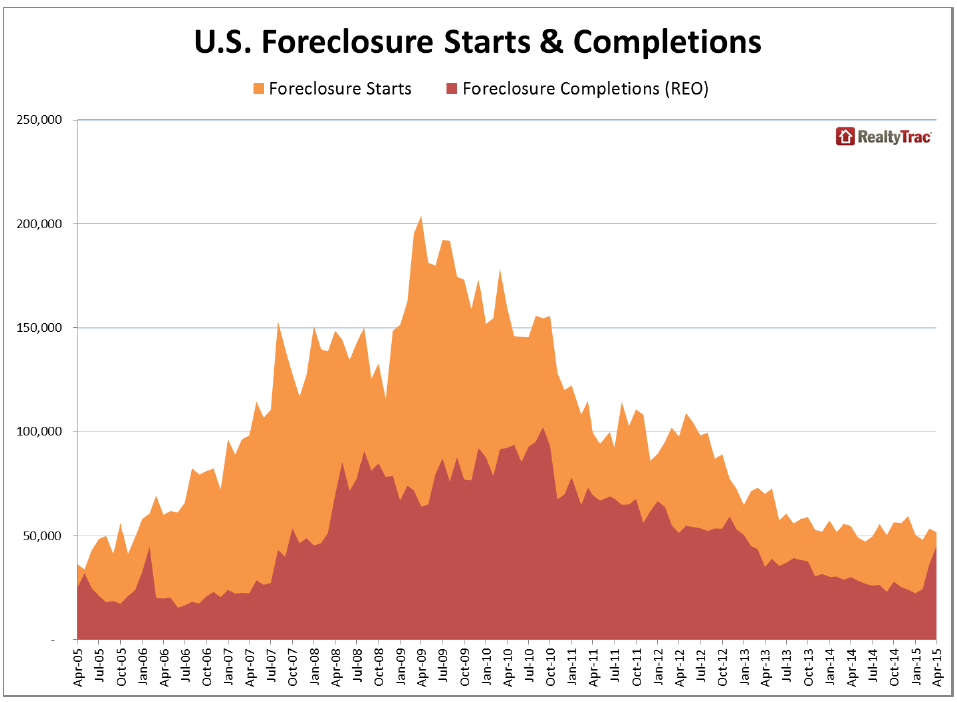

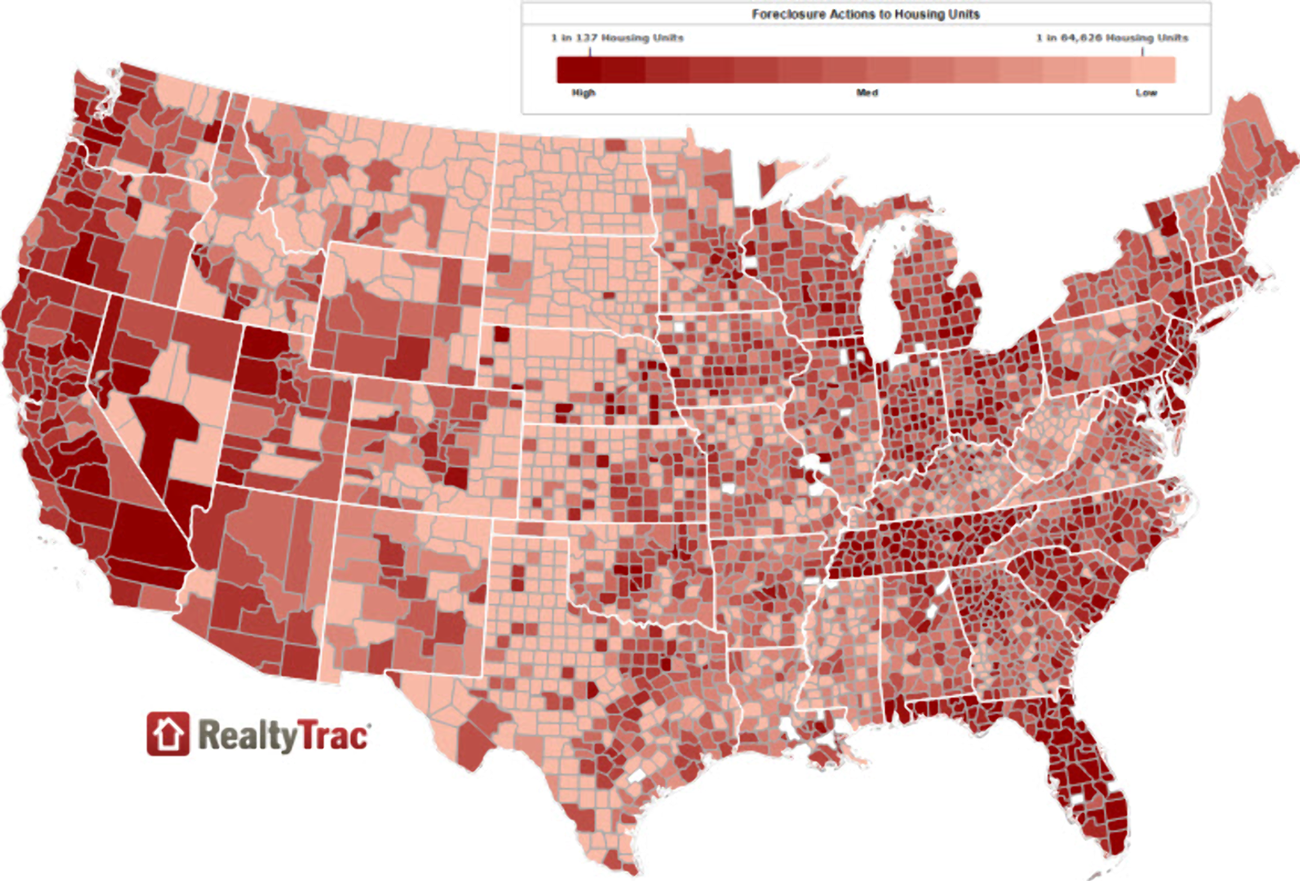

Bank Repossessions in U.S. at 27-Month High in April

According to RealtyTrac's April 2015 U.S. Foreclosure Market Report, U.S. foreclosure filings -- default notices, scheduled auctions and bank repossessions -- were reported on 125,875 U.S. properties in April of 2015, up 3 percent from the previous month and up 9 percent from a year ago, an 18-month high. The U.S. foreclosure rate in April was one in every 1,049 housing units with a foreclosure filing.

The increase in April was driven primarily by a jump in bank repossessions (REOs), which at 45,168 were up 25 percent from the previous month and up 50 percent from a year ago to a 27-month high. REOs increased on a year-over-year basis for the second consecutive month. The spike in April REOs is still 56 percent below the peak of 102,134 REOs in September 2013. (Also see special methodology note on REO data collection below.)

"The REO increase in April was foreshadowed by a 23-month high in scheduled foreclosure auctions in October 2014," said Daren Blomquist, vice president at RealtyTrac. "Many of those scheduled auctions are now taking place, and properties are going back to the foreclosing lender. Meanwhile we continue to see foreclosure starts decrease, and foreclosure starts nationwide are now running consistently below pre-crisis levels -- indicating that the overall increase in foreclosure activity in April is a continuation of the clean-up phase of the last housing crisis, not the start of a new crisis.

"While distressed sales typically have a stifling effect on the housing market, in this particular market an influx of distressed inventory could actually help stimulate sales during the spring and summer buying season as new listings become available, often in the middle to lower ranges of the market," Blomquist added. "Banks are liquidating these distressed properties in a seller's market with a low supply of inventory for sale, which should help them sell quickly and at a price that is relatively close to full market value."

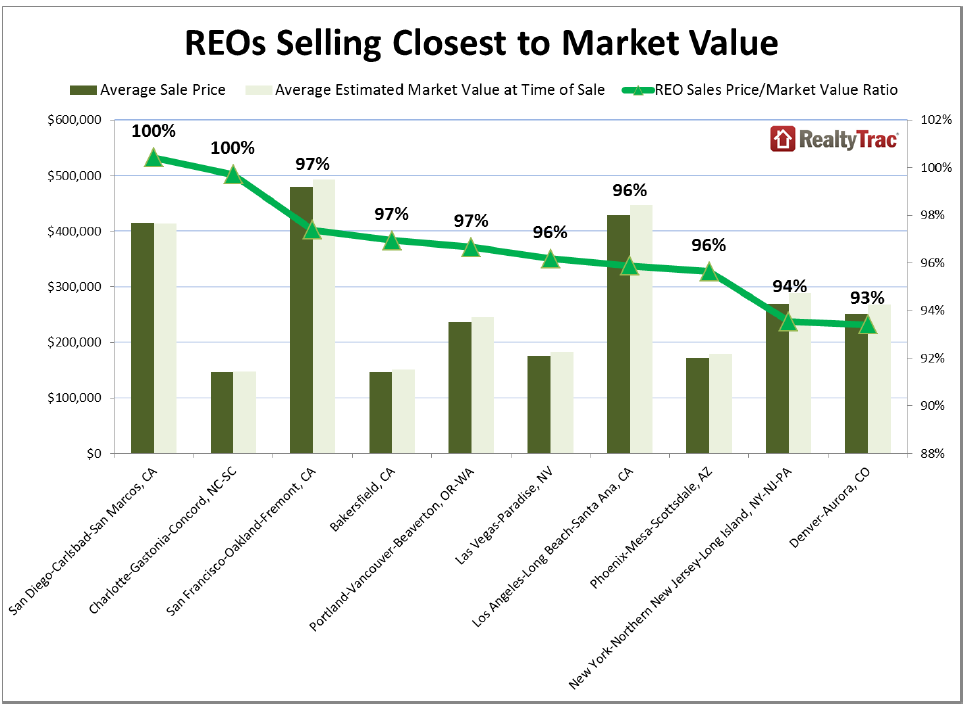

REOs sold for 87 percent of estimated market value in first quarter

The average sale price of REOs sold in the first quarter was 87 percent of the average estimated market value of those same properties at the time of sale. In some markets REOs sold at a much higher price-to-value ratio, including San Diego, California (100 percent), Charlotte, North Carolina (100 percent), San Francisco, California (97 percent), Bakersfield, Carolina (97 percent) and Portland, Oregon (97 percent).

"We've seen distressed inventory work its way through the auction and REO process at a varying pace depending on local market conditions and price points," said Mark Hughes, chief operating officer with First Team Real Estate, covering the Southern California market. "The uptick in April is a natural part of that flow toward equilibrium and a more stable market."

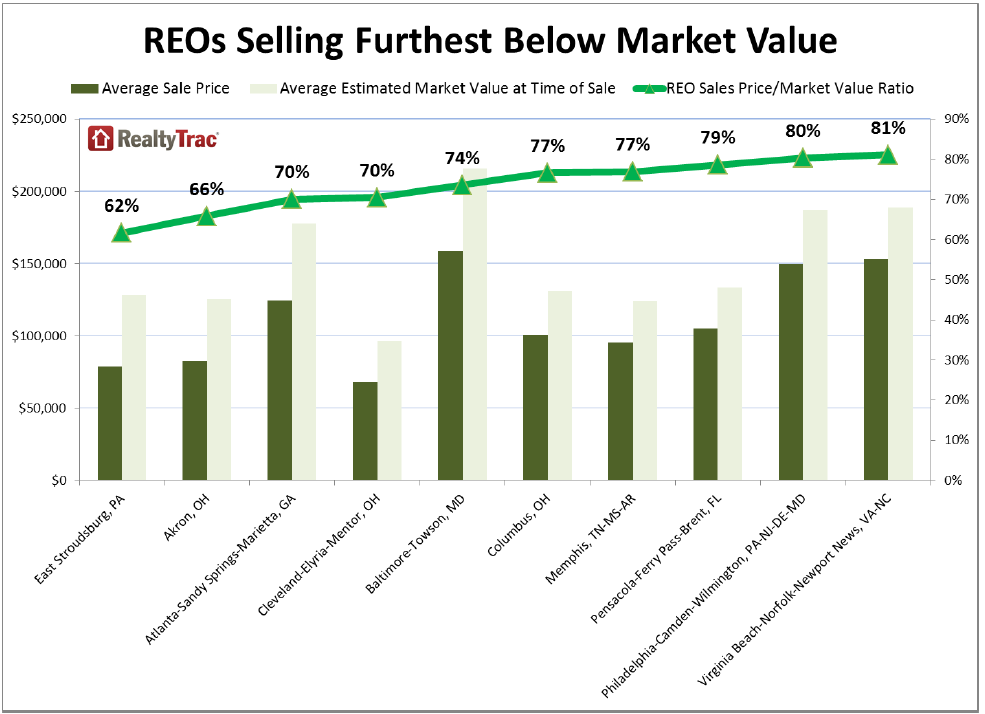

Markets where REOs sold for the lowest price-to-value ratio in the first quarter were East Stroudsburg, Pennsylvania (62 percent), Akron, Ohio (66 percent), Atlanta (70 percent), Cleveland (70 percent), and Baltimore (74 percent).

"While overall foreclosure activity remains lower across Ohio, concerns in a number of communities remain focused on lack of job growth as a potential indicator of increased foreclosure activity for the future," said Michael Mahon, president at HER Realtors, covering the Cincinnati, Dayton and Columbus markets in Ohio. "Areas such as Dayton and Cleveland, that have documented lower than expected job growth numbers for 2015, have maintained a notable increase in REO activity worth monitoring and consideration for potential future trends."

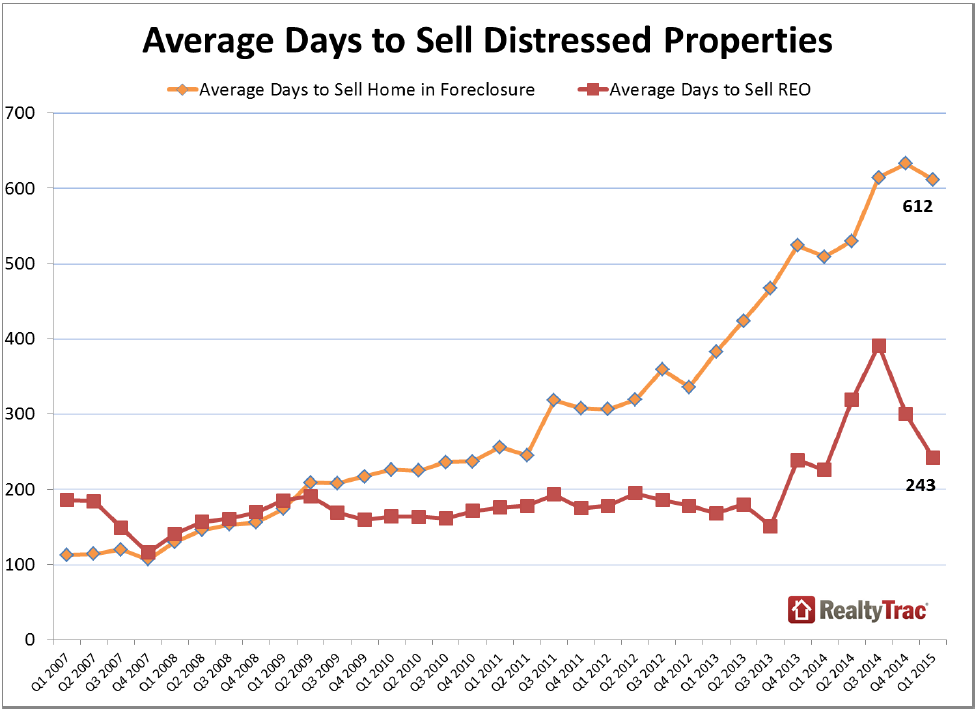

REOs sold in first quarter an average of 243 days after bank repossession

REO properties that sold in the first quarter sold an average of 243 days after being repossessed via foreclosure, down from an average of 300 days for REOs sold in the fourth quarter of 2014 but up from an average of 226 days for REOs sold in the first quarter of 2014.

33 states post annual increase in REOs

Following the national trend, 33 states posted a year-over-year increase in REOs, including Florida (up 42 percent), California (up 53 percent), Michigan (up 198 percent), Illinois (up 46 percent), and Ohio (up 63 percent).

Foreclosure starts down for the fourth consecutive month

A total of 51,773 U.S. properties started the foreclosure process for the first time in April 2015, down 3 percent from the previous month and down 5 percent from a year ago -- the fourth consecutive month with a year-over-year increase in foreclosure starts nationwide. Despite the decrease nationwide, 18 states posted a year-over-year increase in foreclosure starts, including Massachusetts (up 91 percent), Nevada (up 64 percent), and New York (up 31 percent).

Scheduled foreclosure auctions decrease

46,777 properties were scheduled for foreclosure auction in April (scheduled foreclosure auctions are foreclosure starts in some states) down 8 percent from the previous month and down 5 percent from a year ago. Despite the decrease nationwide, 21 states posted year-over-year increases in scheduled foreclosure auctions, including New York (up 82 percent), Massachusetts (up 33 percent), Nevada (up 31 percent) and New Jersey (up 22 percent).

Florida posts highest state foreclosure rate

Despite a 6 percent year-over-year decrease in foreclosure filings, Florida still had the highest state foreclosure rate in April: one in every 425 housing units with a foreclosure filing -- nearly 2.5 times the national average.

"We are in the final innings of this extra-inning distressed ball game," said Mike Pappas, CEO and president of the Keyes Company, covering the South Florida market. "As this tide recedes the strong economic tide is pushing us to historic sales for our region."

Other states with foreclosure rates among the top four highest nationwide posted increases in foreclosure activity: Nevada at No. 2 with foreclosure activity up 39 percent year-over-year; Maryland at No. 3 with foreclosure activity up 5 percent year-over-year; and New Jersey at No. 4 with foreclosure activity up 18 percent year-over-year.

Metros with the highest foreclosure rates

Of metro areas with a population of over 200,000, those with the highest foreclosure rates were Atlantic City, New Jersey (one in every 297), Jacksonville, Florida (one in every 341), Tampa, Florida (one in every 372), Daytona-Deltona Beach-Ormond Beach, Florida (one in every 378) and Miami, Florida (one in every 386).

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More