Commercial Real Estate News

Third-Party Logistics Providers Drive U.S. Big-Box Warehouse Leasing Activity

Based on new data from CBRE, third-party logistics (3PL) providers leased more big-box (200,000 sq. ft. or larger) warehouse space in North America than any other occupier category. Accounting for 41% of all big-box lease transactions in 2022, 3PLs expanded their footprints and claimed the largest share for the first time since CBRE began tracking the activity in 2012.

3PLs typically operate companies' logistics and warehousing operations on a contractual basis, gaining efficiencies by handling that work for multiple clients simultaneously. As a result of enduring pandemic-era shifts, companies have expanded their reliance on 3PL partners to create resilient supply chains and economically address customer needs.

The previous leader in big-box leasing activity - retailers and wholesalers - fell to second place, taking 35.8% of the leasing share. Food and beverage occupiers were a distant third, accounting for 8.7% of leasing activity.

"During the pandemic, companies relied on partnerships with 3PLs to stabilize their operations and accommodate demand," said John Morris, CBRE's President of Americas Industrial & Logistics. "The initial thought was that companies would eventually return to self-reliance for their fulfillment needs, but more companies have since realized that 3PLs can play a vital role in their business models, and demand is stronger than ever."

CBRE analyzed warehouses of 200,000 sq. ft. and larger because warehouses of that size are used for large-scale national and international product distribution. Encompassing the United States, Mexico and Canada, the big-box report found that industrial facilities had record-low vacancy rates and unprecedented rent growth in 2022, despite record new construction deliveries. Demand was driven primarily by a desire to serve markets with growing populations, modernize space for automation and improve supply chain resilience.

Matching 2021's record low, the 2022 direct vacancy rate was 3.3% at year-end, which supported first-year base rents growth of 23% year-over-year. With demand for space at a high, and little space available, a record 455 million sq. ft. is currently under construction, of which 25.3% is pre-leased.

"Slower demand at a time of robust construction will result in higher vacancy as time goes on. That will provide relief for occupiers looking for space in a very tight market. New construction will moderate this year, particularly with the financing market so tight. This should lead to double-digit rent growth as construction deliveries slows," explained Mr. Morris.

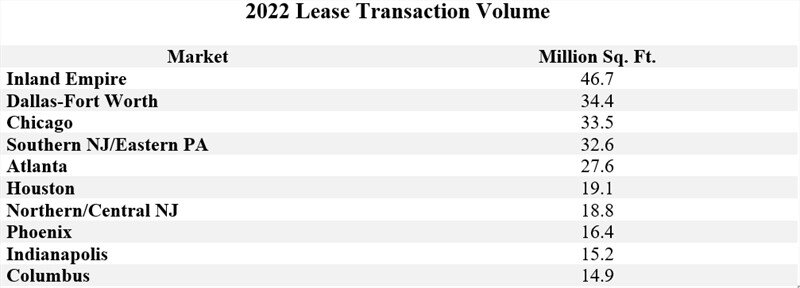

CBRE's report examined 25 big-box markets in North America. Four of these markets had vacancies of less than 1%: Inland Empire (0.1%), Los Angeles County (0.6%), Toronto (0.8%) and Savannah (0.9%).