The WPJ

Residential Real Estate News

U.S. Housing Markets Nationwide Close Out 2017 With Dip in Sales

According to the National Association of Realtors, existing U.S. home sales subsided in most of the country in December, but 2017 as a whole edged up 1.1 percent and ended up being the best year for sales in 11 years.

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, increased 1.1 percent in 2017 to a 5.51 million sales pace and surpassed 2016 (5.45 million) as the highest since 2006 (6.48 million).

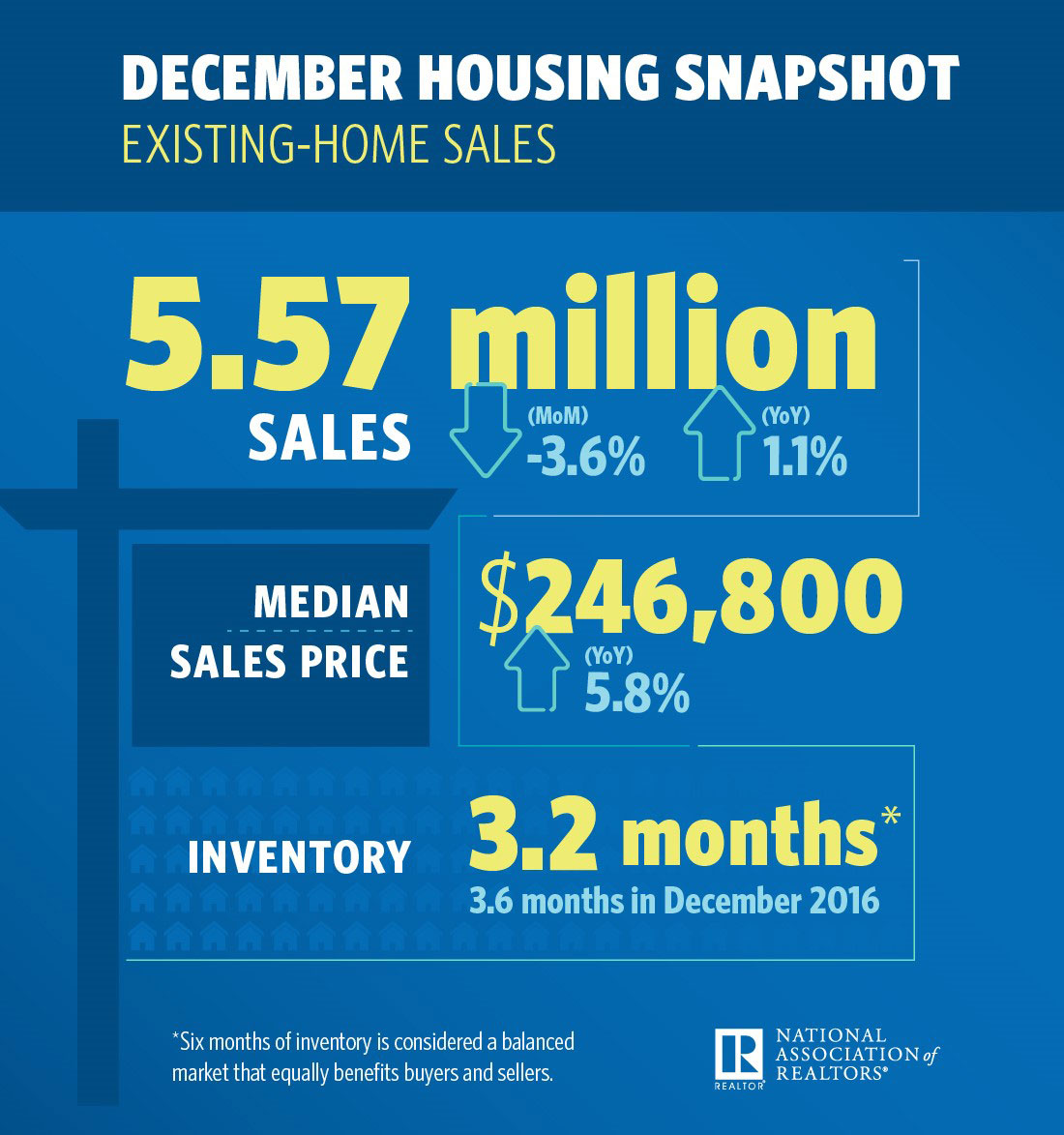

In December, existing-home sales slipped 3.6 percent to a seasonally adjusted annual rate of 5.57 million from a downwardly revised 5.78 million in November. After last month's decline, sales are still 1.1 percent above a year ago.

Lawrence Yun, NAR chief economist, says the housing market performed remarkably well for the U.S. economy in 2017, with substantial wealth gains for homeowners and historically low distressed property sales. "Existing sales concluded the year on a softer note, but they were guided higher these last 12 months by a multi-year streak of exceptional job growth, which ignited buyer demand," said Yun. "At the same time, market conditions were far from perfect. New listings struggled to keep up with what was sold very quickly, and buying became less affordable in a large swath of the country. These two factors ultimately muted what should have been a stronger sales pace."

Added Yun, "Closings scaled back in most areas last month for this same reason. Affordability pressures persisted, and the pool of interested buyers at the end of the year significantly outweighed what was available for sale."

The median existing-home price for all housing types in December was $246,800, up 5.8 percent from December 2016 ($233,300). December's price increase marks the 70th straight month of year-over-year gains.

Total housing inventory at the end of December dropped 11.4 percent to 1.48 million existing homes available for sale, and is now 10.3 percent lower than a year ago (1.65 million) and has fallen year-over-year for 31 consecutive months. Unsold inventory is at a 3.2-month supply at the current sales pace, which is down from 3.6 months a year ago and is the lowest level since NAR began tracking in 1999.

"The lack of supply over the past year has been eye-opening and is why, even with strong job creation pushing wages higher, home price gains - at 5.8 percent nationally in 2017 - doubled the pace of income growth and were even swifter in several markets," said Yun.

First-time buyers were 32 percent of sales in December, which is up from 29 percent in November and unchanged from a year ago. NAR's 2017 Profile of Home Buyers and Sellers - released in late 2017 - revealed that the annual share of first-time buyers was 34 percent.

According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage inched higher for the third straight month to 3.95 percent in December from 3.92 percent in November. The average commitment rate for all of 2017 was 3.99 percent.

"Rising wages and the expanding economy should lay the foundation for 2018 being the turning point towards an uptick in sales to first-time buyers," said Yun. "However, if inventory conditions fail to improve, higher mortgage rates and prices will further eat into affordability and prevent many renters from becoming homeowners."

Properties typically stayed on the market for 40 days in December, which is unchanged from November and down from a year ago (52 days). Forty-four percent of homes sold in December were on the market for less than a month.

Realtor.com's Market Hotness Index, measuring time-on-the-market data and listings views per property, revealed that the hottest metro areas in December were San Jose-Sunnyvale-Santa Clara, Calif.; San Francisco-Oakland-Hayward, Calif.; Vallejo-Fairfield, Calif.; Colorado Springs, Colo.; and Stockton-Lodi, Calif.

NAR President Elizabeth Mendenhall, says improving the new tax law is a top priority for Realtors in 2018. "Especially in high-cost, high-taxed markets, there's still big concern that the overall structure of the final bill diminishes the tax benefits of homeownership in a way that would adversely affect home values and sales over time," she said. "As the housing market adjusts to the new law, Realtors will be listening to their clients and communicating to lawmakers ways to ensure owning a home is truly incentivized in the tax code."

All-cash sales were 20 percent of transactions in December, which is down from 22 percent in November and 21 percent a year ago. Individual investors, who account for many cash sales, purchased 16 percent of homes in December, up from 14 percent both last month and a year ago. For the year, all-cash sales averaged 21 percent of sales (23 percent in 2016), and investor sales were at 15 percent (14 percent in 2016).

Distressed sales - foreclosures and short sales - were 5 percent of sales in December, up from 4 percent in November but down from 7 percent a year ago. Four percent of December sales were foreclosures and 1 percent were short sales.

Single-family and Condo/Co-op Sales

Single-family home sales declined 2.6 percent to a seasonally adjusted annual rate of 4.96 million in December from 5.09 million in November, but are still 1.0 percent above the 4.91 million pace a year ago. The median existing single-family home price was $248,100 in December, up 5.8 percent from December 2016.

Existing condominium and co-op sales fell 11.6 percent to a seasonally adjusted annual rate of 610,000 units in December, but are still 1.7 percent above a year ago. The median existing condo price was $236,500 in December, which is 6.4 percent above a year ago.

Regional Breakdown

December existing-home sales in the Northeast fell 7.5 percent to an annual rate of 740,000, and are now 2.6 percent below a year ago. The median price in the Northeast was $261,400, which is 3.0 percent above December 2016.

In the Midwest, existing-home sales dipped 6.3 percent to an annual rate of 1.33 million in December, but are still 1.5 percent above a year ago. The median price in the Midwest was $191,400, up 7.8 percent from a year ago.

Existing-home sales in the South decreased 1.7 percent to an annual rate of 2.30 million in December, but are still 3.1 percent higher than a year ago. The median price in the South was $221,200, up 5.8 percent from a year ago.

Existing-home sales in the West declined 1.6 percent to an annual rate of 1.20 million in December, and are now 0.8 percent below a year ago. The median price in the West was $367,400, up 7.3 percent from December 2016.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More