Residential Real Estate News

Active U.S. Residential Listings Spike 22 Percent in December

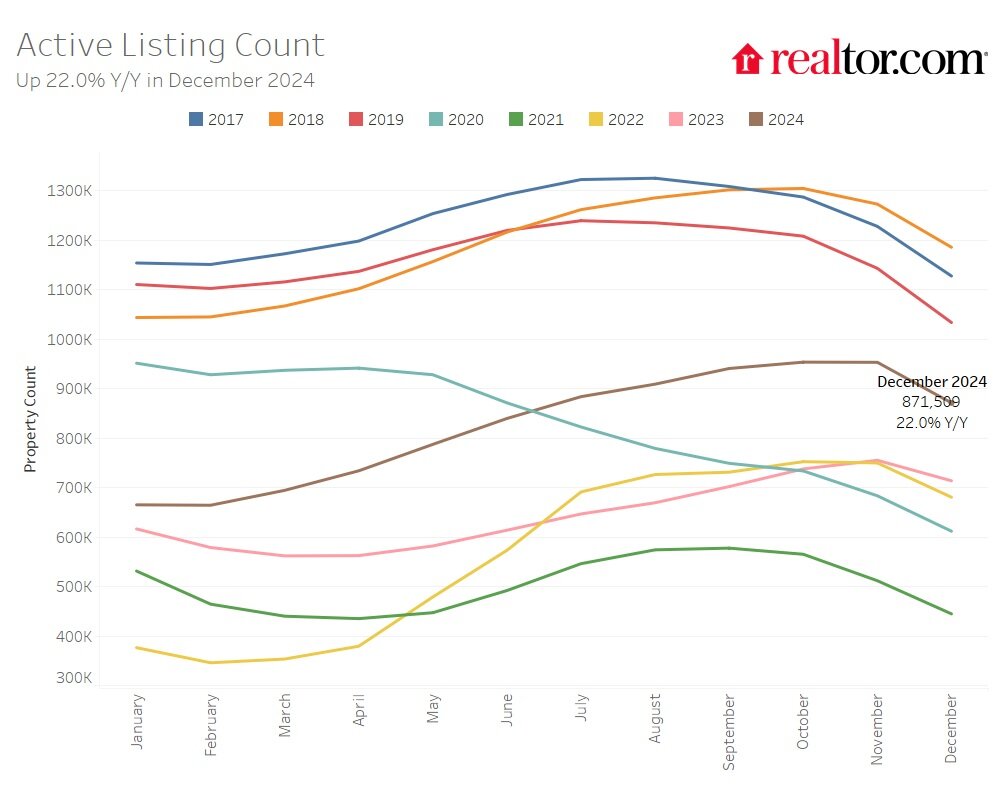

According to Realtor.com, the number of homes actively for sale in the U.S. grew by 22% in December 2024 compared to the previous year, marking the 14th consecutive month of growth. However, seasonal trends caused inventory levels to drop to their lowest point since June 2024.

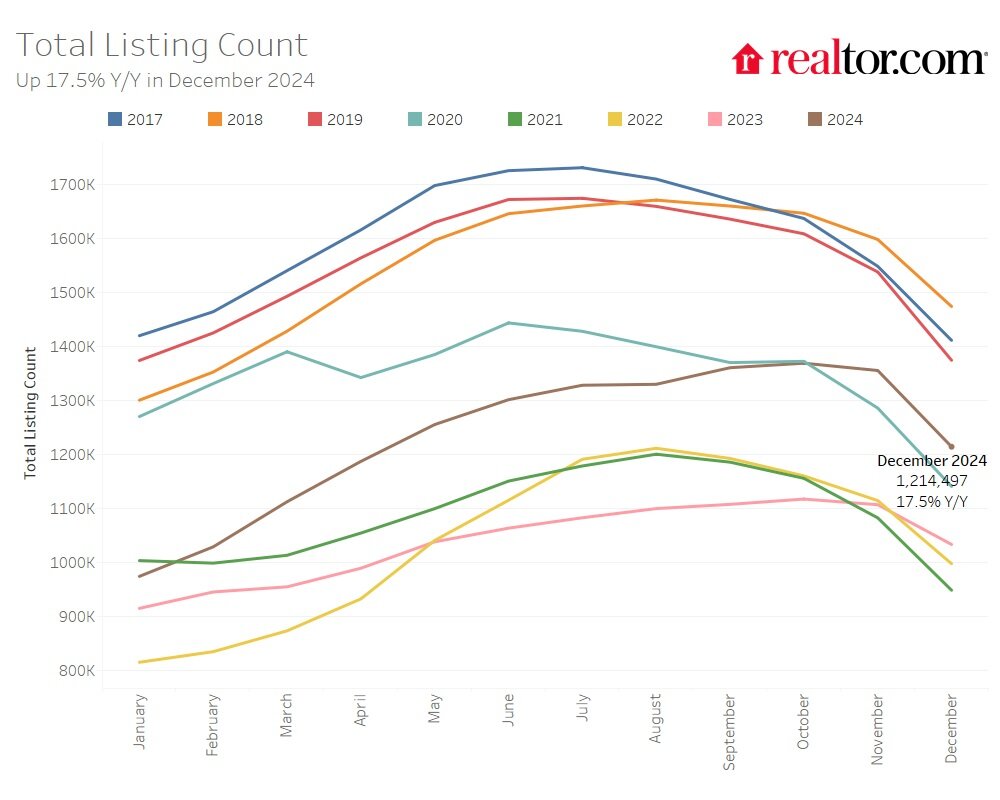

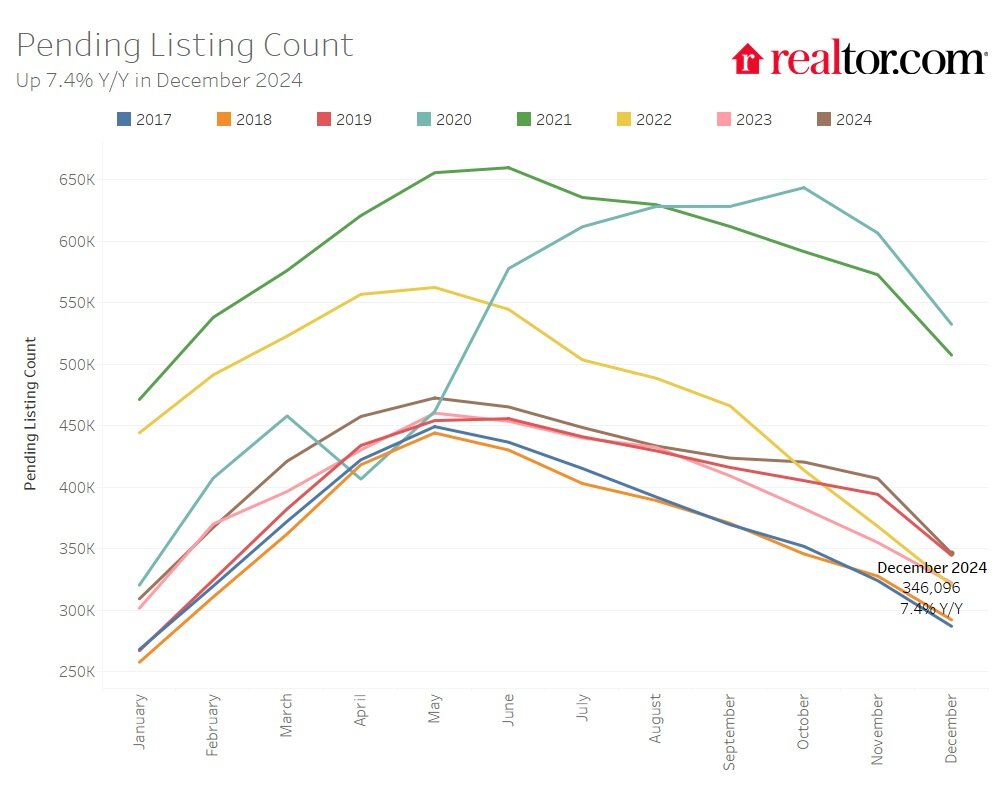

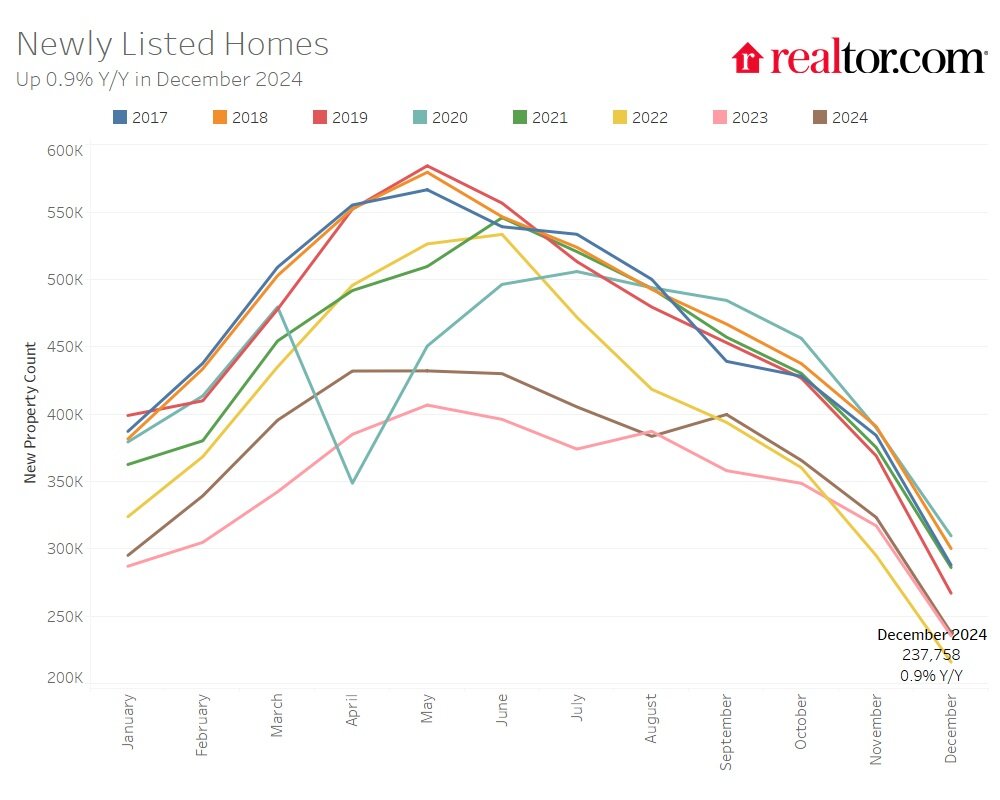

Total unsold homes, including pending sales, increased by 17.5% year-over-year, representing the 12th straight month of annual growth. This growth was slower than November's 22.5%. New listings rose slightly by 0.9% year-over-year, a decrease from November's 2% increase.

The median list price decreased by 1.8% year-over-year to $402,502, while the price per square foot rose by 1.3%, reflecting a growing share of smaller, more affordable homes in the market. Compared to December 2019, list prices have risen by 34.2%, and the price per square foot has increased by 49.5%, says Realtor.com.

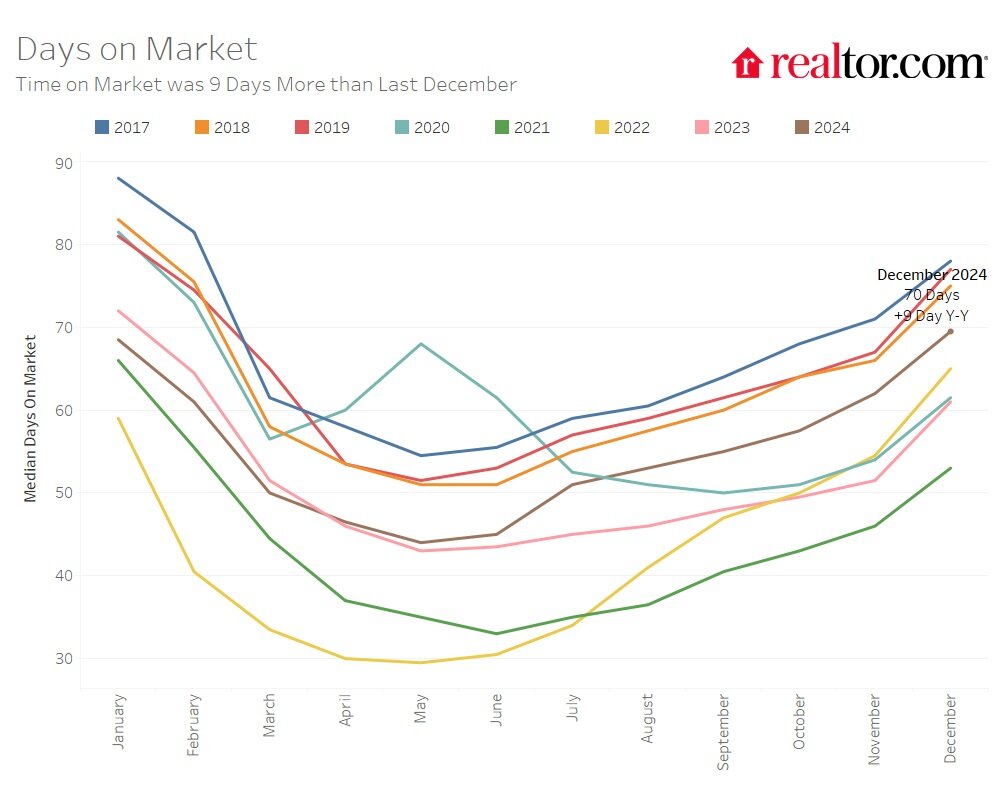

Homes spent an average of 70 days on the market in December, which is nine days longer than last year and eight days longer than November. Despite this slowdown, homes are still selling eight days faster than the pre-pandemic December average from 2017 to 2019.

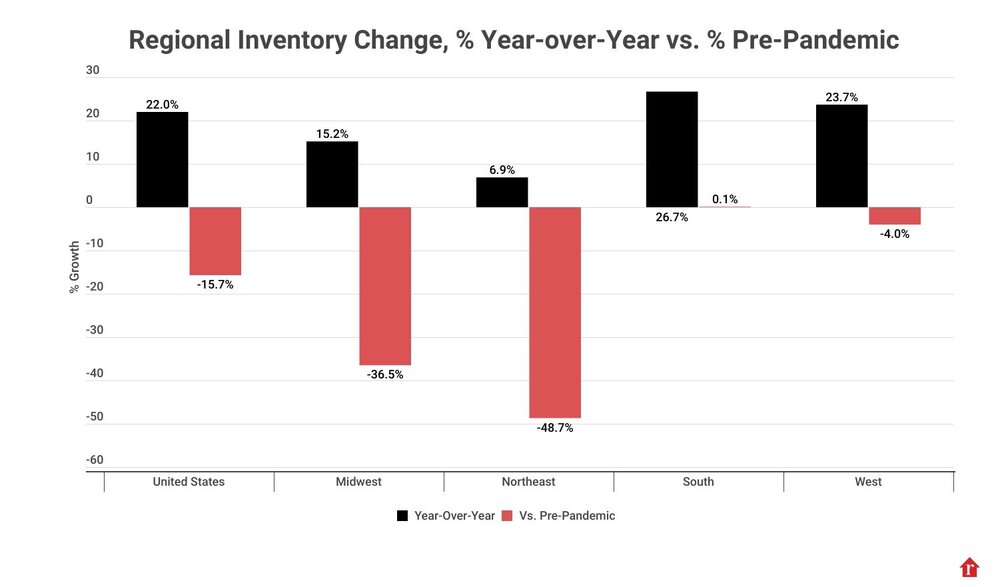

Active inventory grew across all regions, with increases of 26.7% in the South, 23.7% in the West, 15.2% in the Midwest, and 6.9% in the Northeast. Compared to pre-pandemic levels, the South's inventory slightly exceeded 2017-2019 averages by 0.1%, while the West, Midwest, and Northeast showed deficits of 4%, 36.5%, and 48.7%, respectively.

Inventory grew in 49 of the 50 largest metro areas, with Miami (45.4%), Orlando (42.4%), and Denver (41.9%) leading. Only 16 metros had higher inventory levels than pre-pandemic, led by Memphis (37.7%), Austin (36.5%), and Orlando (34.9%).

Price reductions were stable at 12.9% of listings, a slight increase from 12.7% last year. This remains 2.4 percentage points higher than the 2017-2019 average. Higher mortgage rates in November and December reduced homebuyer power, slowing market activity. Modest growth in home sales (1.5%) is expected in 2025 as rates stabilize.

Realtor.com reports listing prices rose slightly in the Midwest (0.7%) and Northeast (0.4%) but declined in the West (-1.3%) and South (-2.3%). The largest metro-level price increases were seen in Cleveland (9.1%), Milwaukee (6.7%), and Detroit (6.2%). Since 2019, the Hartford and New York metros have seen the highest price-per-square-foot growth at 66.8%, while San Francisco (17.9%) and San Jose (24.0%) lagged.

Homes in the South and West spent an additional 10 and 8 days on the market, respectively, compared to last year, while the Midwest and Northeast saw increases of 4 and 5 days. Nationally, 46 of the 50 largest metros experienced longer market times compared to last year, with the biggest increases in Nashville (22 days), Orlando (21 days), and Rochester (21 days).