The WPJ

Commercial Real Estate News

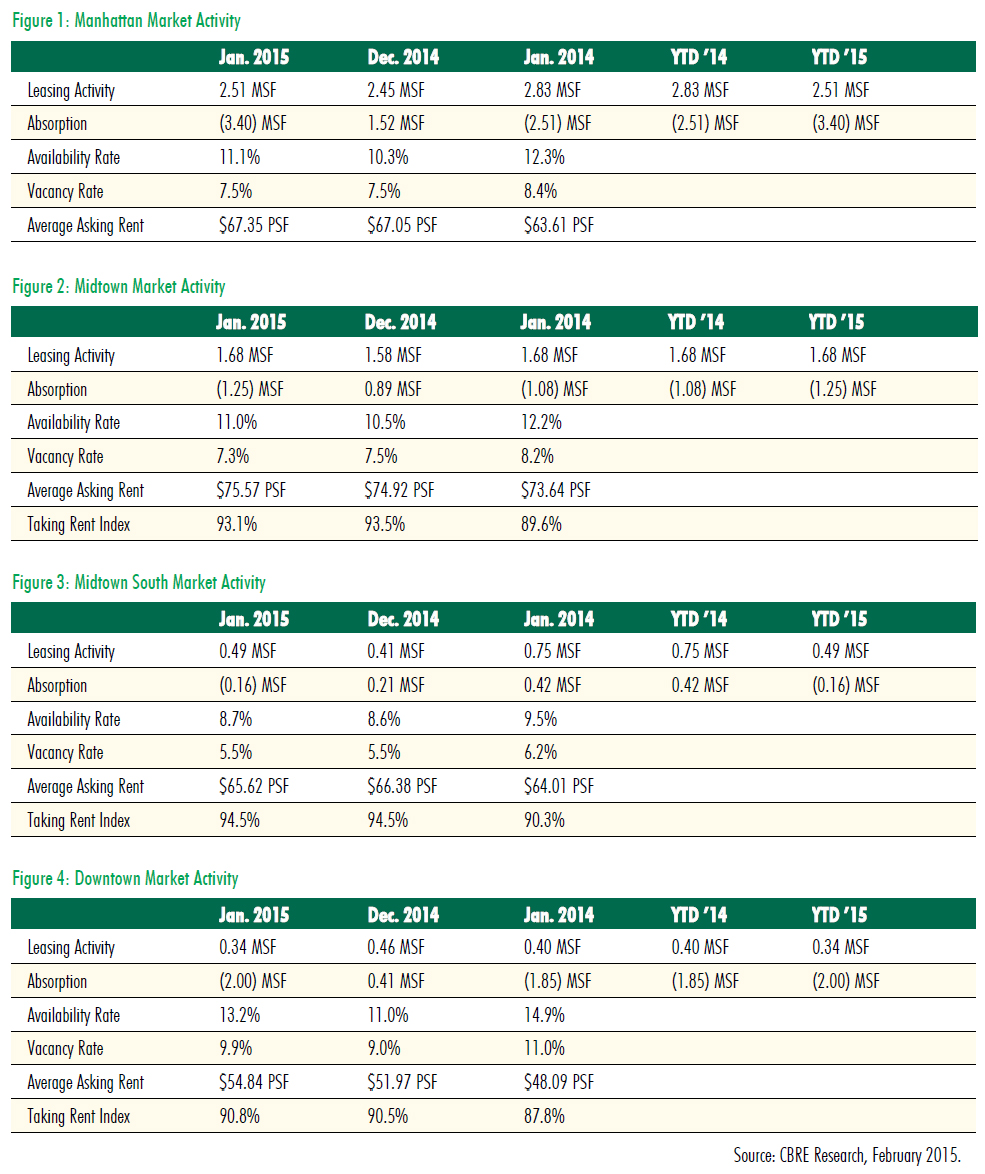

Manhattan Office Asking Rents Up 6% Over Last Year

According to CBRE's February 2015 Manhattan Office MarketView Snapshot Report, Manhattan's office leasing activity totaled 2.51 million square feet during January 2015, 16% higher than the five-year monthly average of 2.16 million sq. ft.

Monthly absorption remained in negative territory due to the annual statistical sample adjustment and large blocks added, ending January at 3.40 million sq. ft. The Manhattan availability rate increased to 11.1% in January, compared to 10.3% in December. The average asking rent finished the month at $67.35 per sq. ft., up 6% from the $63.61 per sq. ft. average reported one year ago.

Manhattan January 2015 office market report highlights include:

Midtown: Leasing activity in January totaled 1.68 million sq. ft., 28% higher than the five-year monthly average of 1.30 million sq. ft., and on par with monthly leasing for January 2014. The largest transaction in Midtown was the renewal and expansion of Kirkland & Ellis LLP at 601 Lexington Avenue. Additions to large blocks of space, as well as the annual statistical adjustment process, largely drove the 1.25 million sq. ft. of negative absorption. The availability rate increased 50 basis points (bps) compared to December, yet decreased 120 bps from one year ago. The average asking rent in January increased $0.65 to end the month at $75.57, up from $74.92 in December and up 3% from a year ago.

Midtown South: Leasing activity in January totaled 0.49 million sq. ft., 17% ahead of the five-year monthly average of 0.42 million sq. ft. All five of the top transactions in this market were new deals, led by the 75,000-sq. ft. expansion of Estée Lauder, Inc., at 28 West 23rd Street. Annual adjustments to the statistical sample, healthy leasing and minimal space additions led to negative absorption of 157,000 sq. ft., the tightest of the three markets. The availability rate increased 10 basis points (bps) compared to December, and dropped 80 bps from one year ago. The average asking rent in January decreased slightly to end the month at $65.62, down from $66.38 in December and up 3% from a year ago.

Downtown: Leasing activity totaled 0.34 million sq. ft., 21% lower than the five-year monthly average of 0.44 million sq. ft. All five of the top transactions in this market were new transactions, led by the 42,000-sq. - ft. new lease by Banco Santander Central Hispano at 200 Liberty Street. The addition of 1.2 million sq. ft. of direct space at 28 Liberty Street (formerly known as 1 Chase Manhattan Plaza) catapulted overall absorption to negative 2.0 million sq. ft. Three additional blocks of space greater than 100,000 sq. ft., which were already on the market but fell with 12 months of possession during January, contributed to this number. The availability rate increased 220 basis points (bps) compared to December, yet decreased 170 bps from one year ago. In addition, at 1.1%, the Downtown market has the lowest sublet availability of the three markets. The average asking rent in January increased to end the month at $54.84, a new record, up from $51.97 in December and up 14% from a year ago.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More