The WPJ

Vacation Real Estate News

Slower Growth Expected for U.S. Hotel Industry in 2017 and 2018

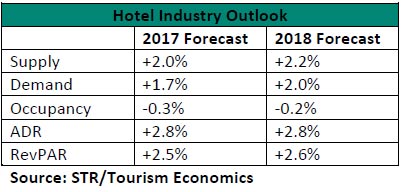

According to STR and Tourism Economics' first forecast of 2017, the U.S. hotel industry is projected to see slower but steady growth through 2018.

"Demand has outpaced supply in terms of growth for seven consecutive years, but we expect that to change in 2017 and continue in 2018," said Amanda Hite, STR's president and CEO. "In an environment where occupancy is flat or slightly declining, ADR is the lone driver of RevPAR, which is why we expect RevPAR growth in 2017 and 2018 to be slower than the industry average of the past 30 years (+3.3%).

"Demand has outpaced supply in terms of growth for seven consecutive years, but we expect that to change in 2017 and continue in 2018," said Amanda Hite, STR's president and CEO. "In an environment where occupancy is flat or slightly declining, ADR is the lone driver of RevPAR, which is why we expect RevPAR growth in 2017 and 2018 to be slower than the industry average of the past 30 years (+3.3%)."That said, growth of any rate continues to push industry performance to all-time highs."

2017

For total-year 2017, the U.S. hotel industry is predicted to report a 0.3% decrease in occupancy to 65.3%, a 2.8% rise in average daily rate (ADR) to US$127.34 and a 2.5% increase in revenue per available room (RevPAR) to US$83.20. RevPAR grew more than 3.0% for each year from 2010 to 2016.

Among Chain Scales, the Midscale segment is expected to see the only year-over-year increase in occupancy (+0.1%). The Independent segment is projected to report the largest increases in ADR (+3.0%) and RevPAR (+2.7%). The lowest rate of overall performance growth is expected in the Upscale segment (RevPAR +1.3%).

2018

For 2018, STR and Tourism Economics project the U.S. hotel industry to report a 0.2% decrease in occupancy to 65.2% but increases in ADR (+2.8% to US$130.95) and RevPAR (+2.6% to US$85.36). All seven Chain Scale segments are expected to see a decrease in occupancy. The Luxury segment is projected to report the largest increases in ADR (+3.0%) and RevPAR (+2.8%).

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More