The WPJ

Residential Real Estate News

First-Time Buyers Earn $30,000 More Than Peers Who Don't

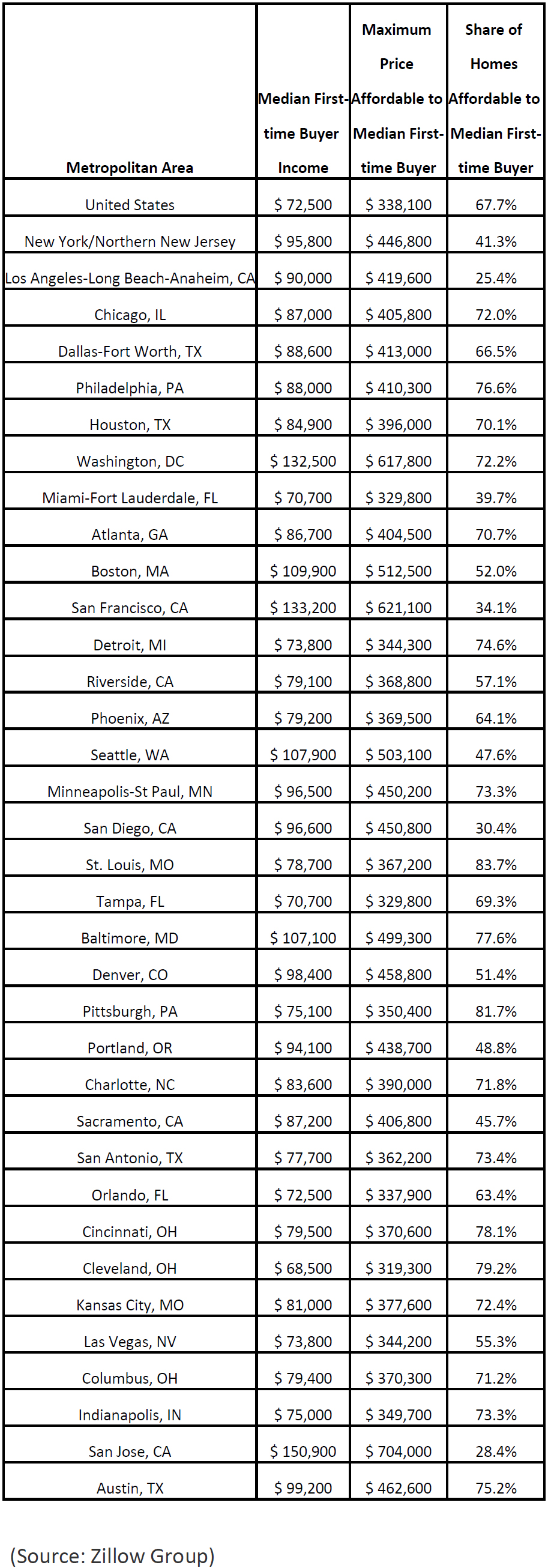

According to the newly released 2018 Zillow Group Report on Consumer Housing Trends, the median income for a first-time buyer in the U.S. is $72,500, compared with the national median household income of $60,700. The difference in income for first-time buyers is more pronounced when compared with their peers who didn't buy, who have a median income of $42,500.

Most buyers rely on savings to finance a down payment, but the second-highest source for a down payment comes from the proceeds from a previous home sale. Buyers entering the market for the first time don't have this resource, though, so a higher income helps them set aside enough for a down payment.

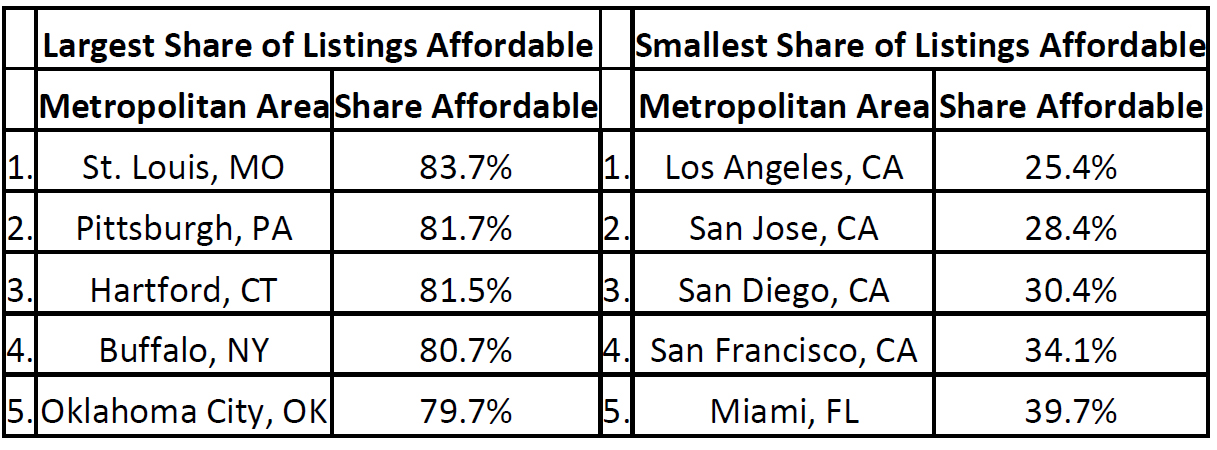

First-time home buyers tend to put down slightly smaller down payments, with a median down payment of 14.5 percent of a home's price, rather than the traditional 20 percent down payment. By comparison, 58 percent of repeat buyers put down at least 20 percent. With this smaller down payment, first-time buyers earning the median income could afford to buy a $338,000 home, meaning they could buy about 68 percent of available homes.

"Buying a home, especially for the first time, is a major step in a lot of people's lives," said Justin LaJoie, RealEstate.com General Manager. "But with home prices climbing ever higher, and inventory yet to see sustained increases, getting a foot in the door is incredibly difficult for new buyers who can't rely on selling another home to come up with a down payment."

These are the markets where first-time buyers can afford the largest and smallest shares of listings

Most buyers rely on savings to finance a down payment, but the second-highest source for a down payment comes from the proceeds from a previous home sale. Buyers entering the market for the first time don't have this resource, though, so a higher income helps them set aside enough for a down payment.

First-time home buyers tend to put down slightly smaller down payments, with a median down payment of 14.5 percent of a home's price, rather than the traditional 20 percent down payment. By comparison, 58 percent of repeat buyers put down at least 20 percent. With this smaller down payment, first-time buyers earning the median income could afford to buy a $338,000 home, meaning they could buy about 68 percent of available homes.

"Buying a home, especially for the first time, is a major step in a lot of people's lives," said Justin LaJoie, RealEstate.com General Manager. "But with home prices climbing ever higher, and inventory yet to see sustained increases, getting a foot in the door is incredibly difficult for new buyers who can't rely on selling another home to come up with a down payment."

These are the markets where first-time buyers can afford the largest and smallest shares of listings

Real Estate Listings Showcase

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More