Residential Real Estate News

Rural Areas in U.S. Lagged Behind Urban Markets in Post-Recession Recovery

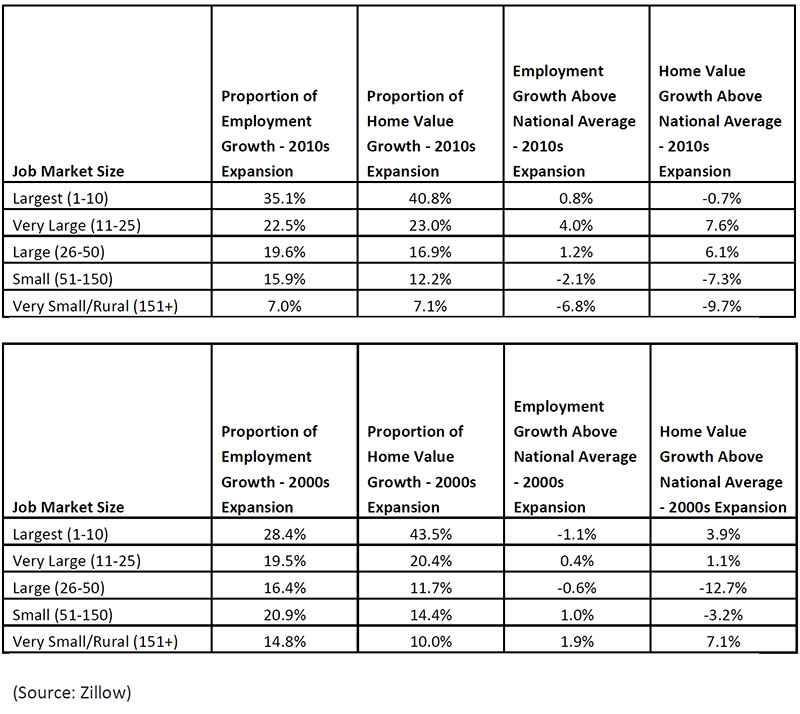

According to Zillow, in the decade following the Great Recession, job growth has been disproportionately concentrated to the largest U.S. job centers, and home values in these markets have risen accordingly. The 25 largest job markets have accounted for more than half of employment growth and nearly two-thirds of home value growth in the U.S. since July 2009.

While housing inventory rose modestly in July, the market has been characterized by persistently low numbers of for-sale homes over the past few years, exacerbating affordability challenges for prospective buyers in many large markets that have experienced strong job growth during the recovery. A combination of concentrated job growth and inventory shortfalls created an environment for dramatic home value appreciation, concentrating home equity accumulation to large markets to an even greater extreme than concentrated job growth alone.

Rapidly rising home values, and a corresponding rise in what's needed for a down payment, are a main reason homeownership rates are lower for young people during the economic expansion than those who reached the same age during or immediately after the Great Recession. Those who graduated from 2007-2010 averaged a homeownership rate of 30.4% four years after graduation, while the classes of 2011-2014 averaged a homeownership rate of 25.3% after the same period despite graduating into a markedly better job market. The pattern holds for non-graduates entering their early 20s - the 2007-2010 group averaged a homeownership rate of 21.1% compared with 18.8% for the 2011-2014 cohort.

Unlike this economic expansion, job growth was strongest in small or rural areas, and home value growth was more aggressive in the very largest and very smallest markets during the previous expansion in the early-to mid-2000s. At that time, rural areas accounted for 14.8% of job growth and home values outperformed the national average by 7.1%. During the expansion since the Great Recession, the proportion of job growth has fallen by more than half to 7%, while housing in rural areas has underperformed the national market by nearly 10%.

"The striking difference between the two periods of recent economic expansion is the contrast between more balanced growth across the U.S. in the early 2000s, to a fairly consistent pattern of rural and small markets being left behind as jobs and home value growth concentrate in large markets," said Skylar Olsen, director of economic research at Zillow. "The jobs story is one of continuing struggles in rural and small markets where manufacturing and agriculture are concentrated. But large cities are seeing another side of the problem in home value growth. It's not only about job vitality but also a city's ability to increase the amount of housing to meet that influx of workers. Job concentration increasingly means that already expensive metros are becoming even more expensive at a faster rate than before."

Growth has been strongest in second-tier markets, ranging from the 11th-largest U.S. job market (Seattle) to the 25th-largest (Pittsburgh). These metros as a whole have outpaced the national average employment growth by 4% and the average home-value growth by 7.6% during this period. Much of this can be attributed to strong growth in a cluster of western areas in this group - Denver (33.5%), Riverside (30.2%), Seattle (24.5%), San Diego (19.2), Phoenix (13.9%) and Portland (10.1%) have each outperformed the national housing market by double digits. Baltimore (-35.2%) and St. Louis (-25.3%) have greatly underperformed compared to the national average.

Housing in the next tier of job markets - ranging from 26th-largest (San Jose) to the 50th-largest (Rochester) - has also performed well, beating the national average home value growth by 6.1%. However, nearly all of this can be attributed to extreme growth in San Jose, which has outpaced the national housing market by a staggering 81.6%. Previous Zillow research has shown that California alone has accounted for nearly one-third of the value gained during this housing recovery.

While housing inventory rose modestly in July, the market has been characterized by persistently low numbers of for-sale homes over the past few years, exacerbating affordability challenges for prospective buyers in many large markets that have experienced strong job growth during the recovery. A combination of concentrated job growth and inventory shortfalls created an environment for dramatic home value appreciation, concentrating home equity accumulation to large markets to an even greater extreme than concentrated job growth alone.

Rapidly rising home values, and a corresponding rise in what's needed for a down payment, are a main reason homeownership rates are lower for young people during the economic expansion than those who reached the same age during or immediately after the Great Recession. Those who graduated from 2007-2010 averaged a homeownership rate of 30.4% four years after graduation, while the classes of 2011-2014 averaged a homeownership rate of 25.3% after the same period despite graduating into a markedly better job market. The pattern holds for non-graduates entering their early 20s - the 2007-2010 group averaged a homeownership rate of 21.1% compared with 18.8% for the 2011-2014 cohort.

Unlike this economic expansion, job growth was strongest in small or rural areas, and home value growth was more aggressive in the very largest and very smallest markets during the previous expansion in the early-to mid-2000s. At that time, rural areas accounted for 14.8% of job growth and home values outperformed the national average by 7.1%. During the expansion since the Great Recession, the proportion of job growth has fallen by more than half to 7%, while housing in rural areas has underperformed the national market by nearly 10%.

"The striking difference between the two periods of recent economic expansion is the contrast between more balanced growth across the U.S. in the early 2000s, to a fairly consistent pattern of rural and small markets being left behind as jobs and home value growth concentrate in large markets," said Skylar Olsen, director of economic research at Zillow. "The jobs story is one of continuing struggles in rural and small markets where manufacturing and agriculture are concentrated. But large cities are seeing another side of the problem in home value growth. It's not only about job vitality but also a city's ability to increase the amount of housing to meet that influx of workers. Job concentration increasingly means that already expensive metros are becoming even more expensive at a faster rate than before."

Growth has been strongest in second-tier markets, ranging from the 11th-largest U.S. job market (Seattle) to the 25th-largest (Pittsburgh). These metros as a whole have outpaced the national average employment growth by 4% and the average home-value growth by 7.6% during this period. Much of this can be attributed to strong growth in a cluster of western areas in this group - Denver (33.5%), Riverside (30.2%), Seattle (24.5%), San Diego (19.2), Phoenix (13.9%) and Portland (10.1%) have each outperformed the national housing market by double digits. Baltimore (-35.2%) and St. Louis (-25.3%) have greatly underperformed compared to the national average.

Housing in the next tier of job markets - ranging from 26th-largest (San Jose) to the 50th-largest (Rochester) - has also performed well, beating the national average home value growth by 6.1%. However, nearly all of this can be attributed to extreme growth in San Jose, which has outpaced the national housing market by a staggering 81.6%. Previous Zillow research has shown that California alone has accounted for nearly one-third of the value gained during this housing recovery.

{kind=link}