The WPJ

Residential Real Estate News

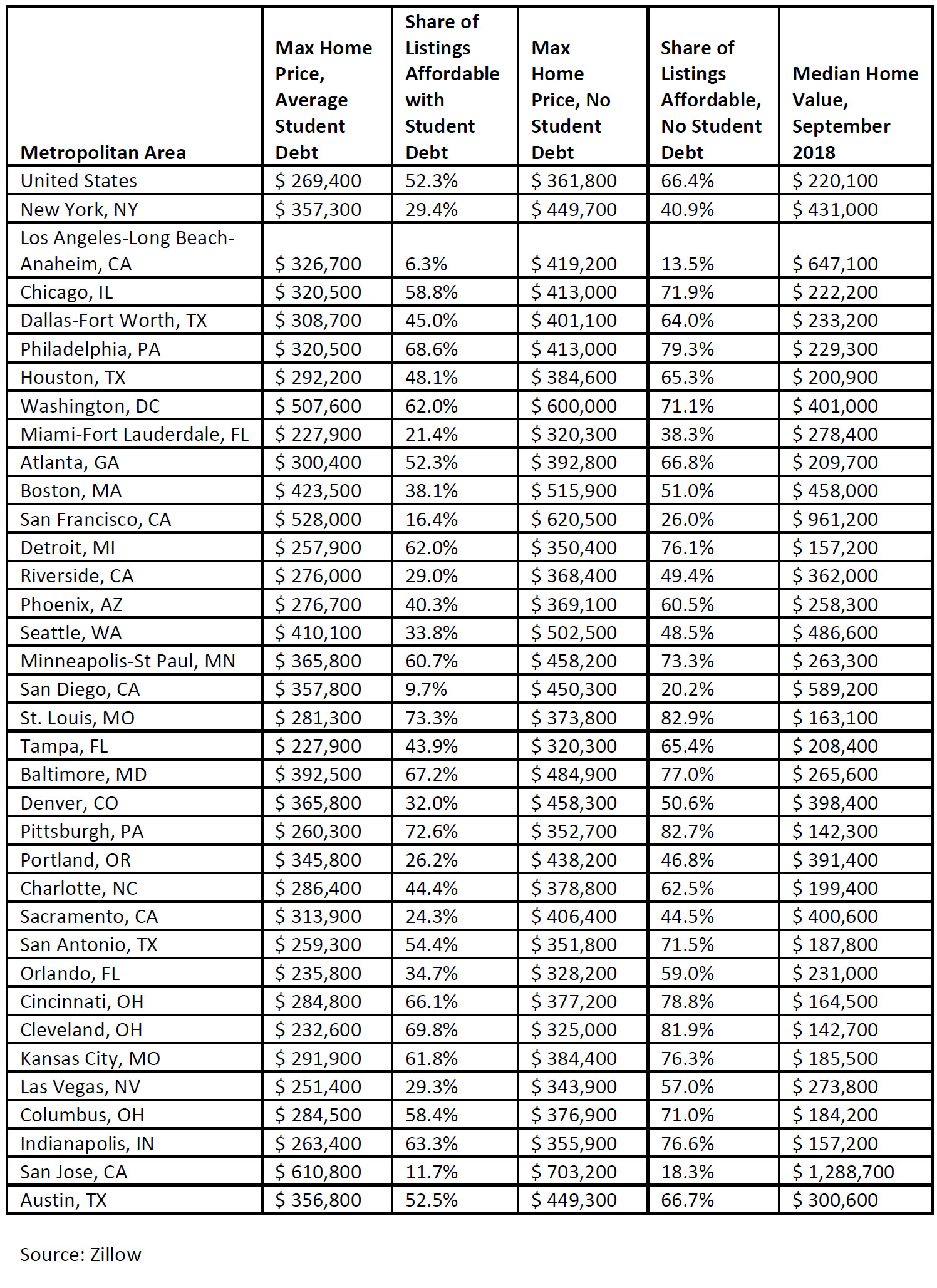

Student Debt in U.S. Reduces Buyers' Budget by $100,000 in 2018

According to new research by Zillow, carrying student debt in the U.S., whether for themselves or someone else, limits potential home buyers' budgets by $92,440, leaving fewer homes on the market they can afford.

The average monthly student debt payment for renters who plan to buy a home in the next year is $388, according to the Zillow Housing Aspirations Report. The maximum priced home a buyer with student debt could afford is $269,400, if they spend no more than 30 percent of their income on combined housing and student debt. At this price point, they could buy 52.3 percent of homes currently listed for sale.

For a buyer with no student debt seeking to spend the same share of income, the buying limit would increase to $361,800, and they could afford to buy 66.4 percent of available homes nationwide.

Student debt reached record levels this year, with the total amount at $1.56 trillion in the third quarter of 2018ii. Paying off student loans also makes it harder to set aside money for a down payment, which is one of the top barriers to homeownership. And saving for that down payment takes longer than it did for previous generations.

"Higher education pays off when it comes to lifetime earnings and the long-term odds of homeownership, but carrying any kind of debt limits how much home buyers can afford. For today's generation of young home buyers, who came of age in a period of rapidly rising education costs, student debt payments can delay the pace of down payment savings and put a dent in their max price point once they do decide to buy," said Zillow Senior Economist Aaron Terrazas. "With for-sale supply still tightest for the most affordable homes but increasingly available at higher prices, even a small reduction in a buyer's target price point can result in substantially fewer options."

Nationwide, about one third (33.9 percent) of renters who are planning to buy a home in the next year have some form of student debt, whether it is for themselves or someone else.

Student debt plays the biggest role in housing affordability in Las Vegas, where buyers with no student debt can afford a much larger share of the homes for sale than those with student debt (57 percent versus 29.3 percent, respectively).

It makes the smallest difference in San Jose, California, where buyers with student debt can afford 11.7 percent of homes, compared with the 18.3 percent of homes that shoppers free from student debt can buy.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More