The WPJ

Residential Real Estate News

Existing Home Sales in U.S. Slightly Uptick in March

According to the National Association of Realtors, existing-home sales in the U.S. grew for the second consecutive month in March 2018, but lagging inventory levels and affordability constraints kept sales activity below year ago levels.

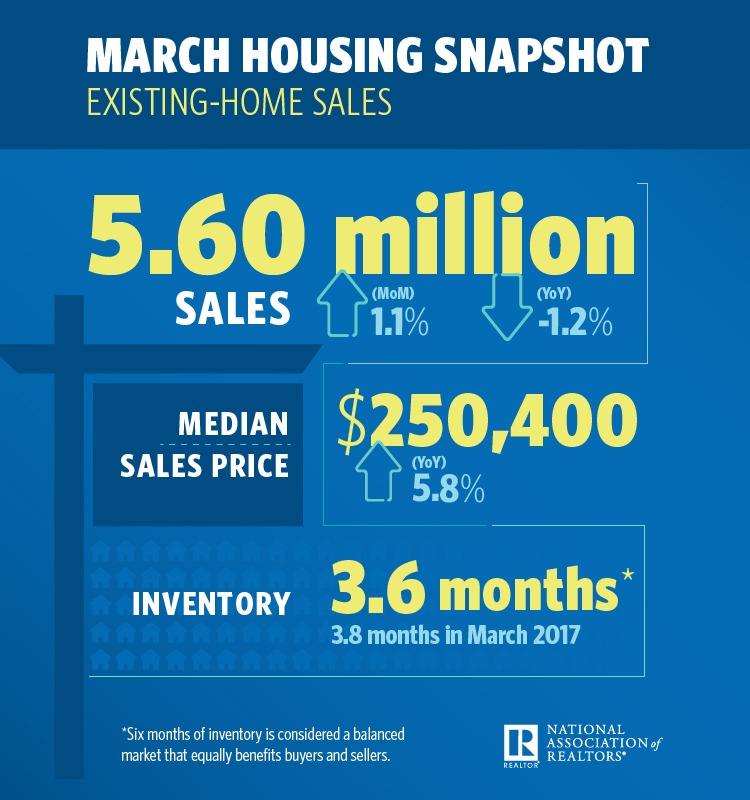

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, rose 1.1 percent to a seasonally adjusted annual rate of 5.60 million in March from 5.54 million in February. Despite last month's increase, sales are still 1.2 percent below a year ago.

Lawrence Yun, NAR chief economist, says closings in March eked forward despite challenging market conditions in most of the country. "Robust gains last month in the Northeast and Midwest - a reversal from the weather-impacted declines seen in February - helped overall sales activity rise to its strongest pace since last November at 5.72 million," said Yun. "The unwelcoming news is that while the healthy economy is generating sustained interest in buying a home this spring, sales are lagging year ago levels because supply is woefully low and home prices keep climbing above what some would-be buyers can afford."

The median existing-home price for all housing types in March was $250,400, up 5.8 percent from March 2017 ($236,600). March's price increase marks the 73rd straight month of year-over-year gains.

"Although the strong job market and recent tax cuts are boosting the incomes of many households, speedy price growth is squeezing overall affordability in several markets - especially those out West," said Yun.

Total housing inventory at the end of March climbed 5.7 percent to 1.67 million existing homes available for sale, but is still 7.2 percent lower than a year ago (1.80 million) and has fallen year-over-year for 34 consecutive months. Unsold inventory is at a 3.6-month supply at the current sales pace (3.8 months a year ago).

According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage increased for the sixth straight month to 4.44 percent in March (highest since 4.46 percent in December 2013) from 4.33 percent in February. The average commitment rate for all of 2017 was 3.99 percent.

Properties typically stayed on the market for 30 days in March, which is down from 37 days in February and 34 days a year ago. Fifty percent of homes sold in March were on the market for less than a month.

"Realtors throughout the country are seeing the seasonal ramp-up in buyer demand this spring but without the commensurate increase in new listings coming onto the market," said Yun. "As a result, competition is swift and homes are going under contract in roughly a month, which is four days faster than last year and a remarkable 17 days faster than March 2016."

Realtor.com's Market Hotness Index, measuring time-on-the-market data and listings views per property, revealed that the hottest metro areas in March were San Francisco-Oakland-Hayward, Calif.; Vallejo-Fairfield, Calif.; Colorado Springs, Colo.; Midland, Texas; and San Jose-Sunnyvale-Santa Clara, Calif.

First-time buyers were 30 percent of sales in March, which is up from 29 percent last month but down from 32 percent a year ago. NAR's 2017 Profile of Home Buyers and Sellers - released in late 2017 - revealed that the annual share of first-time buyers was 34 percent.

NAR President Elizabeth Mendenhall says the extremely tight inventory in the entry-level segment of the market should greatly benefit homeowners looking to trade up this spring. "First-time buyers continue to make up an underperforming share of the market because there are simply not enough homes for sale in their price range," she said. "Supply conditions improve in higher up price brackets, which means those trading up should see considerable interest in their home, as well as more listings to choose from during their own search."

All-cash sales were 20 percent of transactions in March, which is down from 24 percent in February and 23 percent a year ago. Individual investors, who account for many cash sales, purchased 15 percent of homes in March, which is unchanged from February and down from 18 percent a year ago.

Distressed sales - foreclosures and short sales - were 4 percent of sales in March, unchanged from February and down from 6 percent a year ago. Three percent of March sales were foreclosures and 1 percent were short sales.

Single-family and Condo/Co-op Sales

Single-family home sales rose inched forward (0.6 percent) to a seasonally adjusted annual rate of 4.99 million in March from 4.96 million in February, but are 1.0 percent below the 5.04 million sales pace a year ago. The median existing single-family home price was $252,100 in March, up 5.9 percent from March 2017.

Existing condominium and co-op sales increased 5.2 percent to a seasonally adjusted annual rate of 610,000 units in March, but are still 3.2 percent below a year ago. The median existing condo price was $236,100 in March, which is 4.8 percent above a year ago.

Regional Housing Breakdown

March existing-home sales in the Northeast jumped 6.3 percent to an annual rate of 680,000, but are still 9.3 percent below a year ago. The median price in the Northeast was $270,600, which is 3.3 percent above March 2017.

In the Midwest, existing-home sales increased 5.7 percent to an annual rate of 1.29 million in March, but are still 1.5 percent below a year ago. The median price in the Midwest was $192,200, up 5.1 percent from a year ago.

Existing-home sales in the South decreased 0.4 percent to an annual rate of 2.40 million in March, but are 0.4 percent above a year ago. The median price in the South was $222,400, up 5.7 percent from a year ago.

Existing-home sales in the West declined 3.1 percent to an annual rate of 1.23 million in March, but are still 0.8 percent above a year ago. The median price in the West was $377,100, up 7.9 percent from March 2017.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More