The WPJ

Residential Real Estate News

Top 5 Reasons for Declining Homeownership in America Revealed

According to findings of a new white paper by the National Association of Realtors titled Hurdles to Homeownership: Understanding the Barriers, despite steadily improving local job markets and historically low mortgage rates, the U.S. homeownership rate is stuck near a 50-year low because of a perverse mix of affordability challenges, student loan debt, tight credit conditions and housing supply shortages.

The research, which was commissioned by NAR, prepared by Rosen Consulting Group, or RCG, and jointly released by the Fisher Center for Real Estate and Urban Economics at the University of California, Berkeley Haas School of Business, identifies five main barriers that have prevented a significant number of households from purchasing a home. They include:

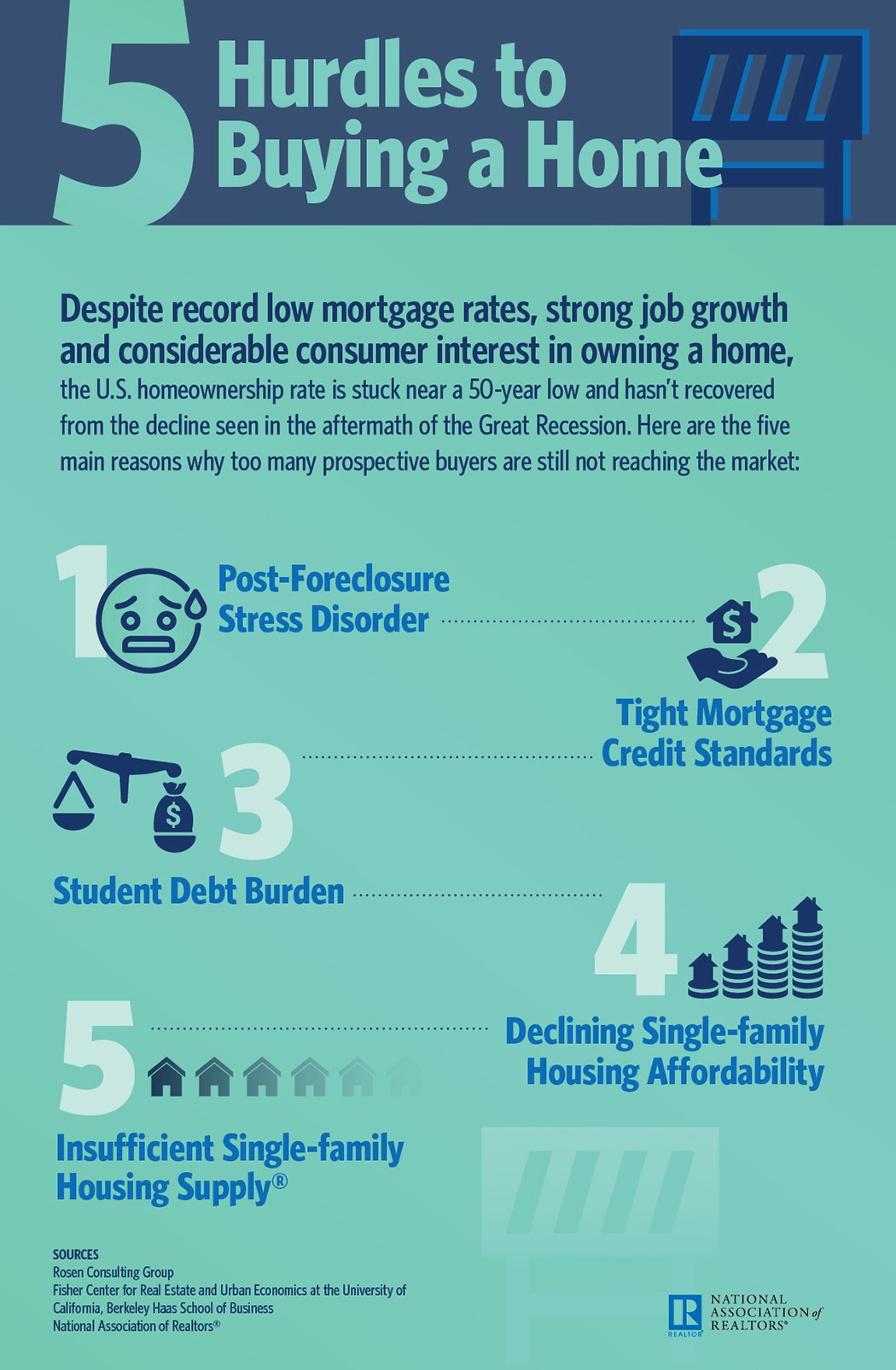

Post-foreclosure stress disorder: There are long-lasting psychological changes in financial decision-making, including housing tenure choice, for the 9 million homeowners who experienced foreclosure, the 8.7 million people who lost their jobs, and some young adults who witnessed the hardships of their family and friends. While most Americans still have positive feelings about homeownership, targeted programs and workshops about financial literacy and mortgage debt could help return-buyers and those who may have negative biases about owning.

Mortgage availability: Credit standards have not normalized following the Great Recession. Borrowers with good-to-excellent credit scores are not getting approved at the rate they were in 2003, prior to the period of excessively lax lending standards. Safely restoring lending requirements to accessible standards is key to helping creditworthy households purchase homes.

The growing burden of student loan debt: Young households are repaying an increasing level of student loan debt that makes it extremely difficult to save for a down payment, qualify for a mortgage and afford a mortgage payment, especially in areas with high rents and home prices. As NAR found in a survey released last year, student loan debt is delaying purchases from millennials and over half expect to be delayed by at least five years. Policy changes need to be enacted that address soaring tuition costs and make repayment less burdensome.

Single-family housing affordability: Lack of inventory, higher rents and home prices, difficulty saving for a down payment and investors weighing on supply levels by scooping up single-family homes have all lead to many markets experiencing decaying affordability conditions. Unless these challenges subside, RCG forecasts that affordability will fall by an average of nearly 9 percentage points across all 75 major markets between 2016 and 2019, with approximately 5 million fewer households able to afford the local median-priced home by 2019. Declining affordability needs to be addressed with policies enacted that ensure creditworthy young households and minority groups have the opportunity to own a home.

Single-family housing supply shortages: "Single-family home construction plummeted after the recession and is still failing to keep up with demand as cities see increased migration and population as the result of faster job growth," said Rosen. "The insufficient level of homebuilding has created a cumulative deficit of nearly 3.7 million new homes over the last eight years."

Fewer property lots at higher prices, difficulty finding skilled labor and higher construction costs are among the reasons cited by RCG for why housing starts are not ramping up to meet the growing demand for new supply. A concentrated effort to combat these obstacles is needed to increase building, alleviate supply shortages and preserve affordability for prospective buyers.

"The decline and stagnation in the homeownership rate is a trend that's pointing in the wrong direction, and must be reversed given the many benefits of homeownership to individuals, communities and the nation's economy," said NAR's 2017 President William E. Brown. "Those who are financially capable and willing to assume the responsibilities of owning a home should have the opportunity to pursue that dream." One of Brown's main objectives as president of NAR is identifying ways to boost the homeownership rate in a safe and responsible way.

"Low mortgage rates and a healthy job market for college-educated adults should have translated to more home sales and upward movement in the homeownership rate in recent years," said Yun. "Sadly, this has not been the case. Obtaining a mortgage has been tough for those with good credit, savings for a down payment are instead going towards steeper rents and student loans, and first-time buyers are finding that listings in their price range are severely inadequate."

Added Rosen, "A healthy housing market is critical to the overall success of the U.S. economy. Too many would-be buyers have been locked out of the market by the factors found in this study, and it's also one of the biggest reasons why economic growth has been subpar in the current recovery."

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More