The WPJ

Residential Real Estate News

Residential Mortgage Delinquencies Increase in U.S.

Yet Foreclosure Starts Continue Decline

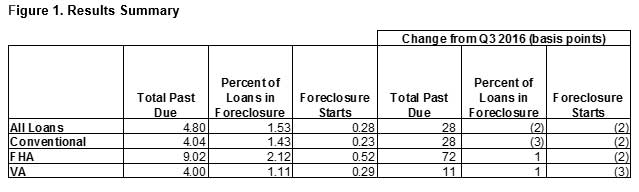

According to the Mortgage Bankers Association's latest National Delinquency Survey, the delinquency rate for mortgage loans on one-to-four-unit U.S. residential properties increased to a seasonally adjusted rate of 4.80 percent of all loans outstanding at the end of the fourth quarter of 2016. The delinquency rate was up 28 basis points from the previous quarter, and was three basis points higher than one year ago.

The percentage of loans on which foreclosure actions were started during the fourth quarter was 0.28 percent, a decrease of two basis points from the previous quarter, and eight basis points lower than one year ago. This is the lowest rate of new foreclosures started since the fourth quarter of 1988.

The delinquency rate includes loans that are at least one payment past due but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the fourth quarter was 1.53 percent, down two basis points from the third quarter and 24 basis points lower than one year ago. This was the lowest foreclosure inventory rate since the second quarter of 2007.

The serious delinquency rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 3.13 percent, an increase of 17 basis points from last quarter, and a decrease of 31 basis points from last year.

Marina Walsh, MBA's Vice President of Industry Analysis, offered the following commentary on the survey:

"We saw a mixed set of results in the most recent survey. Mortgage delinquencies increased in the fourth quarter for the first time since 2013, while both new foreclosure starts and the percentage of loans in foreclosure continued to decline.

"The overall delinquency rate in the fourth quarter increased across all loan types - FHA, VA and conventional - as compared to the third quarter. However, it should be noted that last quarter's overall delinquency rate was at its lowest level since 2006. It is not unexpected that delinquencies could eventually increase off such a low base. We continue to see strong fundamentals in the overall economy, such as rising home values and increased employment, which bodes well for the future performance of FHA, VA and conventional loans.

"The seasonally-adjusted FHA delinquency rate increased to 9.02 percent in the fourth quarter from 8.30 percent in the third quarter (its lowest level since 1997). This quarter's increase was driven primarily by the FHA 30-day delinquency category, which increased 55 basis points over the quarter. The increase in early stage FHA delinquencies was led by loans made in 2014, 2015 and 2016. However, on a year-over-year basis, there was no increase in the overall FHA delinquency rate.

"The seasonally adjusted VA delinquency rate increased to 4.00 percent in the fourth quarter from 3.89 percent in the third quarter (its lowest level since 1979). On a year-over-year basis, the VA delinquency rate declined 12 basis points.

"The seasonally adjusted conventional delinquency rate increased to 4.04 percent in the fourth quarter from 3.76 percent in the third quarter. On a year-over-year basis, the conventional delinquency rate increased by 6 basis points.

"The foreclosure starts rate decreased two basis points to its lowest level since 1988. Foreclosure starts in the fourth quarter decreased across all loan types - FHA, VA and conventional. The overall foreclosure inventory dropped by two basis points, and remained at its lowest level since 2007.

"At the state level, 47 states and DC had no change or a decrease in foreclosure starts in the fourth quarter, while 22 states saw either no change or a decrease in loans in foreclosure. New Jersey and New York continued to have the highest percentage of loans in foreclosure, at 5.42 percent and 4.28 percent, but also continued to show improvement from the previous quarter.

"The serious delinquency rate, which captures the percentage of loans that are 90 days or more past due or in the process of foreclosure, increased to 3.13 percent from 2.96 percent in the third quarter, when the rate was at its lowest level since 2007. The increase in the fourth quarter was driven by an increase in loans 90+ days past due, even though loans in foreclosure continued to decrease. Over 70 percent of seriously delinquent loans were attributable to loans originated in 2007 and earlier."

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More