The WPJ

Residential Real Estate News

U.S. Home Sales Slide in April

Days on Market Falls to Under a Month

According to the National Association of Realtors, stubbornly low supply levels held down existing-home sales in April 2017 and also pushed the median number of days a home was on the market to a new low of 29 days.

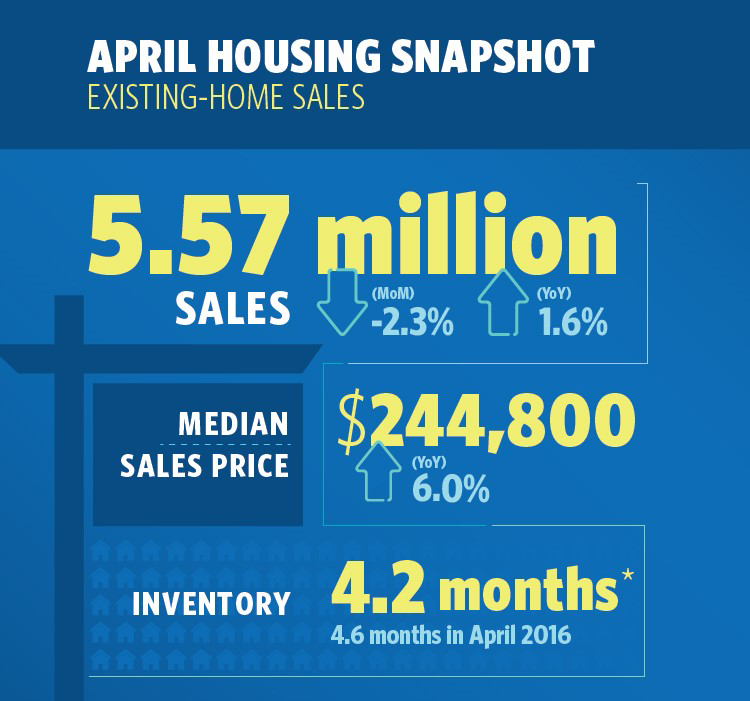

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, dipped 2.3 percent to a seasonally adjusted annual rate of 5.57 million in April from a downwardly revised 5.70 million in March. Despite last month's decline, sales are still 1.6 percent above a year ago and at the fourth highest pace over the past year.

Lawrence Yun, NAR chief economist, says every major region except for the Midwest saw a retreat in existing sales in April. "Last month's dip in closings was somewhat expected given that there was such a strong sales increase in March at 4.2 percent, and new and existing inventory is not keeping up with the fast pace homes are coming off the market," he said. "Demand is easily outstripping supply in most of the country and it's stymieing many prospective buyers from finding a home to purchase."

The median existing-home price for all housing types in April was $244,800, up 6.0 percent from April 2016 ($230,900). April's price increase marks the 62nd straight month of year-over-year gains.

Total housing inventory at the end of April climbed 7.2 percent to 1.93 million existing homes available for sale, but is still 9.0 percent lower than a year ago (2.12 million) and has fallen year-over-year for 23 consecutive months. Unsold inventory is at a 4.2-month supply at the current sales pace, which is down from 4.6 months a year ago.

"Realtors continue to voice the frustration their clients are experiencing because of the insufficient number of homes for sale," added Yun. "Homes in the lower- and mid-market price range are hard to find in most markets, and when one is listed for sale, interest is immediate and multiple offers are nudging the eventual sales prices higher."

Properties typically stayed on the market for 29 days in April, which is down from 34 days in March and 39 days a year ago, and surpasses last May (32 days) as the shortest timeframe since NAR began tracking in May 2011. Short sales were on the market the longest at a median of 88 days in April, while foreclosures sold in 46 days and non-distressed homes took 28 days. Fifty-two percent of homes sold in April were on the market for less than a month (a new high).

Inventory data from realtor.com reveals that the metropolitan statistical areas where listings stayed on the market the shortest amount of time in April were San Jose-Sunnyvale-Santa Clara, Calif., 23 days; San Francisco-Oakland-Hayward, Calif., 25 days; Denver-Aurora-Lakewood, Colo., 27 days; and Seattle-Tacoma-Bellevue, Wash., 28 days.

According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage declined for the first time in six months, dipping to 4.05 percent in April from 4.20 percent in March. The average commitment rate for all of 2016 was 3.65 percent.

"Mortgage rates have been stuck in a holding pattern in recent months, which is a relief for spring homebuyers," said Yun. "With price growth showing little sign of slowing, prospective first-time buyers will be the most sensitive to any sudden uptick in rates in the months ahead."

Matching the highest percentage since last September, first-time buyers were 34 percent of sales in April, which is up from 32 percent both in March and a year ago. NAR's 2016 Profile of Home Buyers and Sellers - released in late 2016 - revealed that the annual share of first-time buyers was 35 percent.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More